By Young Americans Insurance Editorial Team

Published on · Updated on

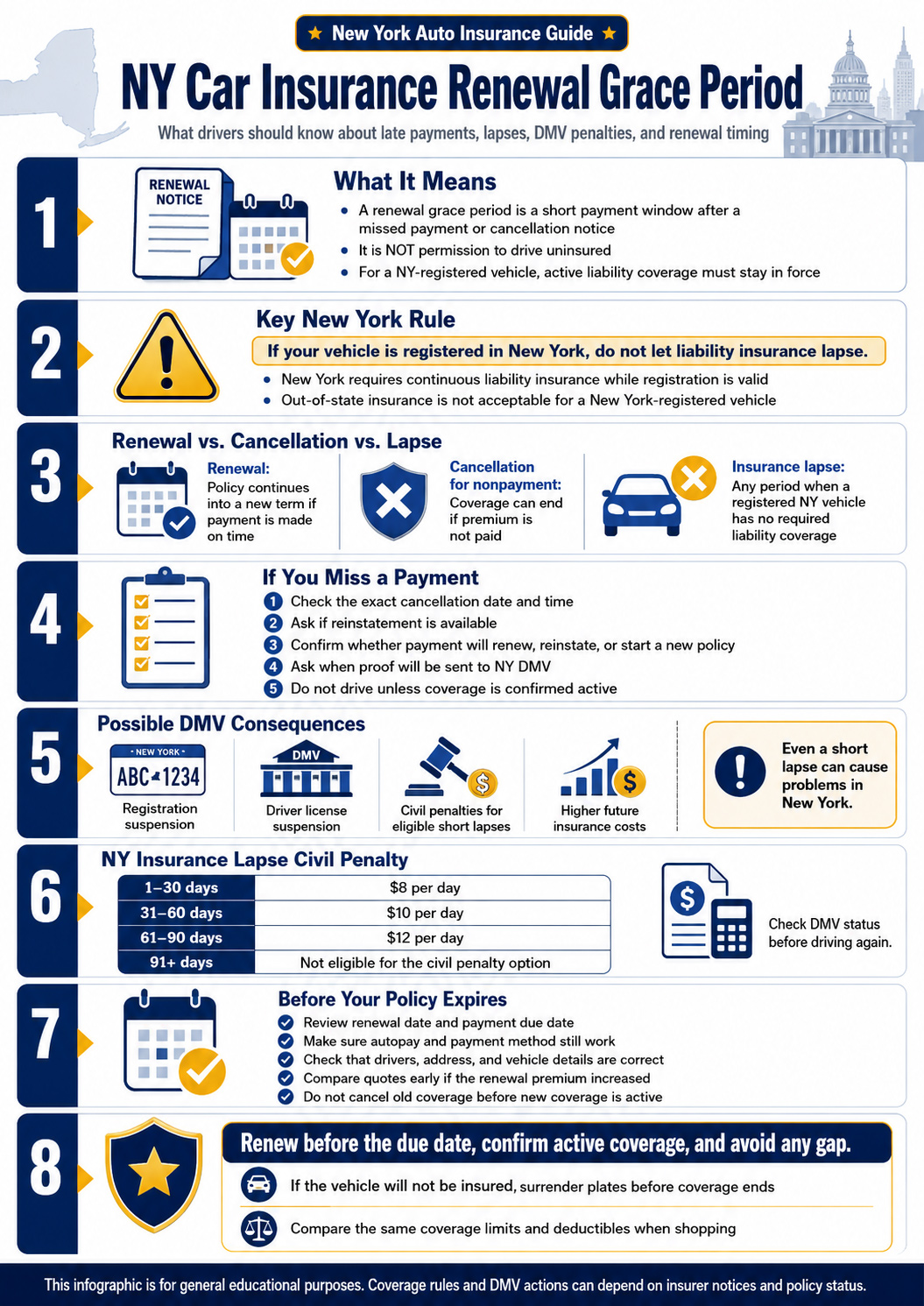

A New York car insurance renewal grace period is not the same as permission to drive without insurance. If your vehicle is registered in New York, your required liability coverage must stay active while the registration is valid.

Missing a renewal payment can lead to cancellation, an insurance lapse, registration problems, license suspension, civil penalties, and higher future premiums. This guide explains how renewal payments, cancellation notices, DMV insurance lapses, and late-payment decisions usually work for New York drivers.

What Is a Car Insurance Renewal Grace Period in NY?

A car insurance renewal grace period is a short window where a policyholder may still be able to pay after a missed payment or cancellation notice. In New York, drivers should be careful with this phrase because there is no safe general rule that lets you keep driving a registered vehicle without active liability insurance.

The New York Department of Financial Services has explained that, for certain covered automobile policies, payment is considered timely if made within 15 days after the insurer mails a cancellation notice for nonpayment of premium.[1] However, that does not mean every driver has unlimited extra time, and it does not remove DMV consequences if coverage actually lapses.

Payment window

New York law can treat payment as timely if it is made within the required period after a cancellation notice for nonpayment.

Not free coverage

A grace period should not be treated as permission to drive if your policy has already canceled or expired.

DMV risk

Any gap between cancellation and new coverage can become an insurance lapse for a New York-registered vehicle.

Does New York Require Continuous Auto Insurance?

Yes. New York DMV says you must keep New York State-issued automobile liability insurance in effect while your vehicle registration is valid, even if you are not using the vehicle. DMV also says out-of-state insurance is never acceptable for a vehicle registered in New York.[2]

DMV defines an insurance lapse as a period of time when there is no liability insurance coverage for a vehicle registered in New York State. According to DMV, any amount of time that a vehicle is registered but not insured can cause a lapse, and DMV can suspend the registration and driver license.[3]

If your vehicle is registered in New York, do not let your liability insurance end before new New York coverage begins or before you properly surrender your plates. DMV summarizes the idea simply: no insurance, no plates.

New York Minimum Car Insurance Requirements

New York requires more than a casual proof-of-insurance card. The coverage must be issued by a company licensed by the New York State Department of Financial Services and certified by New York DMV. Your insurance and registration names must match, and DMV must receive electronic notice from the insurer as well as valid proof of insurance.[4]

| Required Coverage Area | New York Minimum | Why It Matters During Renewal |

|---|---|---|

| Property damage liability | $10,000 for property damage in a single crash | Your policy must continue to meet New York’s required liability standards. |

| Bodily injury liability | $25,000 for bodily injury to one person and $50,000 for bodily injury to two or more people | A renewal quote with lower required protection would not satisfy New York’s minimum requirements. |

| Death liability | $50,000 for death of one person and $100,000 for death of two or more people | New York’s required limits include separate death benefit amounts. |

| No-fault coverage | Mandatory no-fault coverage of $50,000 | DFS says mandatory no-fault coverage is required in New York.[5] |

Renewal, Cancellation, Non-Renewal, and Lapse: What Is the Difference?

These terms are often confused, but they mean different things. Understanding the difference can help you avoid assuming you still have coverage when you do not.

| Term | What It Usually Means | Why NY Drivers Should Care |

|---|---|---|

| Renewal | The insurer offers to continue coverage for another policy term, often with a new premium and due date. | You may need to pay before the renewal effective date to keep coverage active. |

| Cancellation for nonpayment | The insurer cancels coverage because the required premium or installment was not paid. | DFS guidance explains payment can be timely if made within the required period after a cancellation notice for nonpayment. |

| Non-renewal | The insurer does not continue the policy after the current term ends. | You need replacement coverage before the old policy ends to avoid a DMV lapse. |

| Insurance lapse | A period where a New York-registered vehicle has no required liability coverage. | DMV can suspend your registration and driver license if there is a lapse. |

The renewal bill, cancellation notice, insurance ID card, DMV letter, and policy declarations page are not the same document. If the dates are confusing, call your insurer or agent before the policy ends.

What Happens If You Miss a Car Insurance Renewal Payment in New York?

If you miss a renewal payment, the result depends on your insurer’s billing rules, policy terms, cancellation notice, and whether the payment is made in time. DFS has explained that insurers may request renewal premium before the renewal effective date and may send a notice of cancellation for nonpayment if the premium is not paid when due.[6]

The safest move is to act before the policy expires or cancels. Do not wait for DMV to contact you. If the insurer already canceled the policy, ask whether reinstatement is available, whether there was any gap, and whether your insurer has reported the cancellation or reinstatement to DMV.

If you missed a renewal payment, do this quickly:

- Check the exact cancellation date and time on the insurer’s notice.

- Ask whether the policy can be reinstated without a gap.

- Pay only after confirming what the payment will do: reinstate, renew, rewrite, or start a new policy.

- Ask when electronic proof will be sent to New York DMV.

- Do not drive if you cannot confirm that coverage is active.

- Save payment receipts, confirmation numbers, emails, and insurance ID cards.

- If the vehicle will not be insured, surrender the plates before coverage ends.

How New York DMV Treats Insurance Lapses

New York DMV says an insurance lapse can occur between the date insurance is canceled and the date new insurance begins, plates are surrendered, registration expires, other valid proof applies, or the insurance company reinstates coverage.[7]

If you do not have valid auto liability insurance, DMV says you must immediately surrender your registration and vehicle plates. DMV also warns that driving without insurance can lead to tickets, impoundment, revocation, suspension, fines, and penalties.[8]

| Situation | Possible DMV Issue | Safer Action |

|---|---|---|

| Your renewal payment was late but the policy is still active | Potential cancellation if payment is not made in time. | Pay immediately and confirm active coverage in writing. |

| Your policy canceled and new coverage started later | Possible insurance lapse for the gap period. | Keep documents showing cancellation, new effective date, and any reinstatement. |

| Your car is registered but uninsured | Registration and license suspension risk. | Surrender plates immediately if coverage will not be active. |

| You bought out-of-state coverage for a New York-registered car | DMV does not accept out-of-state insurance for NY-registered vehicles. | Replace it with New York State-issued coverage from an accepted insurer. |

New York Insurance Lapse Civil Penalties

New York DMV may allow some drivers to pay an insurance lapse civil penalty instead of surrendering plates, but only in limited situations. DMV says you can pay and remove a suspension if the lapse is 90 days or less. You cannot pay if you already paid a civil penalty in the past 36 months or if the lapse is 91 days or more.[9]

| Insurance Lapse Length | DMV Civil Penalty | Important Note |

|---|---|---|

| 1–30 days | $8 per day | DMV calculates the amount based on the number of lapse days. |

| 31–60 days | $10 per day | The rate increases after the first 30 days. |

| 61–90 days | $12 per day | DMV lists 90 days as the maximum lapse length eligible for civil penalty payment. |

| 91 days or more | Not eligible for the civil penalty option | DMV says you cannot pay the civil penalty if the lapse is 91 days or more. |

DMV says paying the civil penalty does not guarantee that DMV restored your registration or closed other suspensions or revocations. Check your status before driving.

Why a New York Insurance Lapse Can Become Expensive

A short lapse can create more than a billing issue. It can affect DMV status, legal driving ability, future premiums, and your ability to register or operate a vehicle. DMV also says that if a registration suspension period is more than 90 days, you must surrender your registration and plates, and DMV will suspend your driver license for the same number of days as the registration suspension. A $50 license suspension termination fee may also apply.[10]

DMV can suspend the vehicle registration when there is a lapse in required liability insurance.

An insurance lapse can also lead to driver license suspension, especially when the lapse is longer.

Civil penalties, reinstatement issues, fees, and higher future premiums can cost more than the missed payment.

If a crash happens while coverage is inactive, the financial consequences can be severe.

What to Do Before Your Policy Expires

The best way to handle a renewal grace period is to avoid needing one. Set reminders before your renewal date, read the bill carefully, and compare alternatives early if the price increased.

Before renewal, check these items:

- Renewal effective date and expiration date.

- Payment due date and accepted payment methods.

- Whether the quoted premium is monthly, six-month, or annual.

- Whether automatic payments are active and the card or bank account is still valid.

- Whether your address, vehicle, drivers, and garaging ZIP code are correct.

- Whether your liability limits, deductibles, collision, comprehensive, rental, and roadside options still fit.

- Whether the insurer will send electronic notice to New York DMV after renewal.

If you are comparing prices before your renewal deadline, review auto insurance options for young drivers and make sure each quote uses the same coverage limits and deductibles.

What to Do If Your Policy Already Lapsed

If your New York policy already lapsed, focus on stopping the problem from getting worse. Do not keep driving while coverage is uncertain. Confirm the cancellation date, ask whether reinstatement is available, and check whether DMV has sent or may send an insurance inquiry letter or suspension order.

| Step | Why It Matters |

|---|---|

| Stop driving until coverage is confirmed | Driving without valid insurance can lead to serious DMV and legal consequences. |

| Call your insurer or agent | Ask whether coverage can be reinstated with no gap or whether a new policy is required. |

| Confirm the exact lapse dates | DMV penalties and suspension issues depend on how long the lapse lasted. |

| Save proof of payment and insurance ID cards | You may need documentation if DMV sends a letter or order. |

| Surrender plates if the vehicle will not be insured | DMV tells drivers to surrender registration and plates if the vehicle does not have valid liability coverage. |

| Check DMV status before driving again | A policy payment does not automatically mean every DMV suspension or revocation has been cleared. |

Can You Switch Insurance Companies at Renewal in New York?

Yes, but the timing has to be handled carefully. The new policy should begin before the old policy ends. If the old policy cancels at 12:01 a.m. and the new policy starts later, that gap can matter. For a New York-registered vehicle, the safer approach is to avoid any uncovered period at all.

Do not cancel the old policy until the new New York policy is active and you have proof of insurance. Ask the new insurer when coverage begins and when the DMV electronic notice will be sent.

If your main issue is the first payment or payment method, you may also compare ways to start car insurance with a checking account or review flexible car insurance payment options before the renewal deadline.

How to Avoid Renewal Grace Period Problems

Most renewal problems happen because of timing, expired payment methods, address issues, ignored notices, or switching companies too late. A few simple habits can reduce the chance of a lapse.

Prevention checklist

- Set renewal reminders 30, 14, and 7 days before the policy expires.

- Keep your mailing address, email, and phone number current with your insurer and DMV.

- Update expired debit cards, credit cards, or bank accounts before autopay runs.

- Open every cancellation, renewal, and DMV insurance letter immediately.

- Compare quotes early if the renewal premium increased.

- Confirm the new policy effective date before canceling old coverage.

- Surrender plates before coverage ends if you will not insure the vehicle.

- Keep proof of insurance and payment confirmations in a safe place.

Frequently Asked Questions About NY Car Insurance Renewal Grace Periods

Is there a car insurance renewal grace period in New York?

There can be a payment window after a cancellation notice for nonpayment, but drivers should not treat it as permission to drive without active insurance. For a New York-registered vehicle, any period without required liability coverage can become a DMV insurance lapse.

Can I drive in New York if my insurance payment is late?

Only drive if you have confirmed that your policy is still active. A late bill, pending payment, or expired card can become serious if the policy has canceled or will cancel before payment is processed.

What happens if my New York car insurance lapses for one day?

DMV says any amount of time that a registered vehicle is not insured can cause a lapse. Even a short gap should be handled carefully with your insurer and DMV.

Can I pay a New York DMV civil penalty instead of surrendering plates?

Sometimes. DMV says you may be able to pay the civil penalty if the lapse is 90 days or less, but not if you paid a civil penalty in the past 36 months or if the lapse is 91 days or more.

Does New York accept out-of-state insurance for a New York-registered car?

No. DMV says out-of-state insurance is not acceptable for a vehicle registered in New York. The coverage must be New York State-issued by an insurer accepted by New York authorities.

Should I cancel my old policy before buying a new one?

No. Make sure the new policy is active first. The safer approach is to avoid any gap between the old policy ending and the new policy beginning.

What should I do if I cannot afford my renewal premium?

Compare quotes before the policy expires, ask your insurer about payment options, review deductibles and optional coverages, and avoid letting the policy cancel while the vehicle is still registered.

Final Thoughts on New York Car Insurance Renewal Grace Periods

A New York car insurance renewal grace period should be treated as a last-chance payment issue, not as extra time to drive uninsured. The safest approach is to renew before the due date, confirm active coverage, and avoid any gap while your vehicle remains registered.

If your renewal premium is too high, compare replacement coverage early. If your policy already canceled, stop driving until coverage and DMV status are clear. In New York, a short lapse can become a registration, license, and financial problem quickly.

Compare Coverage Before Your Renewal Deadline

If your New York renewal premium increased or your payment deadline is close, compare options before your current policy expires. Match the same coverage limits, deductibles, drivers, and vehicle details before choosing a new policy.

Compare Auto Insurance OptionsReferences

- New York Department of Financial Services, OGC Opinion No. 00-12-02: Automobile Renewal and Cancellation Provisions. Source ↩

- New York DMV, New York State Insurance Requirements. Source ↩

- New York DMV, Insurance Lapses. Source ↩

- New York DMV, New York State Insurance Requirements. Source ↩

- New York Department of Financial Services, How much auto insurance must I carry? Source ↩

- New York Department of Financial Services, OGC Opinion No. 00-12-02: Automobile Renewal and Cancellation Provisions. Source ↩

- New York DMV, Insurance Lapses. Source ↩

- New York DMV, Insurance Lapses. Source ↩

- New York DMV, Pay an Insurance Lapse Civil Penalty. Source ↩

- New York DMV, Insurance Lapses. Source ↩