By Young Americans Insurance Editorial Team

Published on · Updated on

This guide was reviewed for young driver insurance accuracy, coverage clarity, quote-comparison usefulness, payment-plan warnings, and consumer disclosure quality.

Editorial details

The Young Americans Insurance Editorial Team creates informational content about U.S. auto insurance, quote comparison, coverage types, young driver costs, discounts, payment options, and policy-shopping decisions.

This article is for general educational purposes only. Coverage availability, prices, discounts, deductibles, payment options, cancellation rules, and policy terms vary by insurer, state, ZIP code, vehicle, driver profile, and selected coverage.

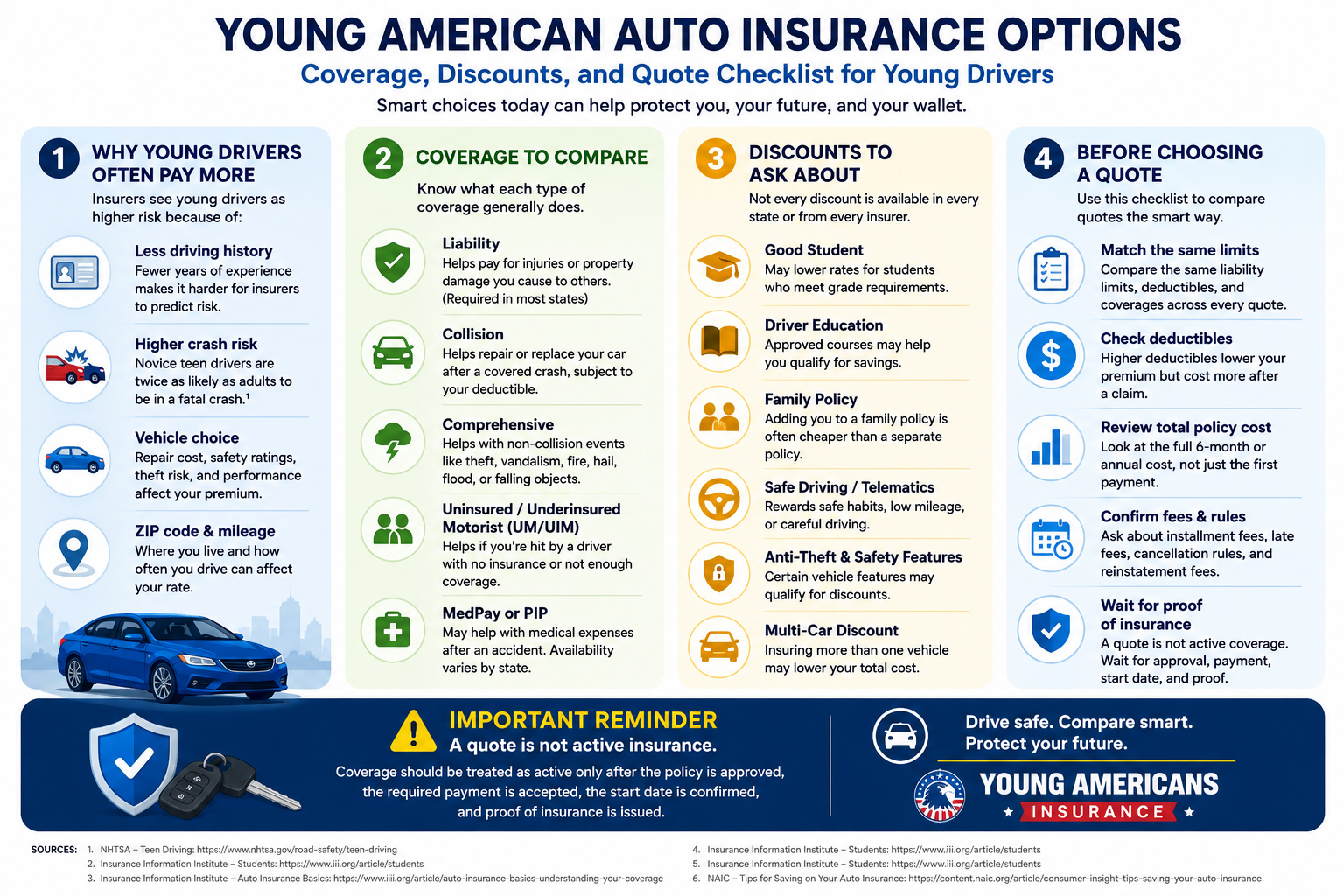

Young American auto insurance shoppers often need help comparing coverage, discounts, payment options, and quote details before choosing a policy. This guide focuses on young drivers, new drivers, students, and growing households that want affordable coverage without overlooking important protection.

Use this page as a practical checklist before comparing quotes: understand why young drivers often pay more, review the major coverage types, ask about discounts, compare the full policy cost, and confirm when coverage actually becomes active.

Quick Summary

- Young drivers often pay more because insurers see less driving history, less experience, and higher crash risk.

- A cheap quote is not always the best quote. Compare liability limits, deductibles, collision, comprehensive, uninsured motorist coverage, payment terms, and total policy cost.

- Teen drivers are often cheaper to insure on a family policy than on a separate policy, but every household should compare both options.

- Good student, driver education, safe driving, family policy, multi-car, anti-theft, and telematics discounts may help eligible drivers lower costs.

- A quote is not active insurance. Coverage should be treated as active only after the policy is approved, the required payment is accepted, the start date is confirmed, and proof of insurance is issued.

Why Auto Insurance Often Costs More for Young Drivers

Young drivers often pay more for car insurance because insurers price policies based on risk. The Insurance Information Institute says teenage drivers are considered the highest-risk segment and can add 50% to 100% to the cost of a family’s auto coverage.[1]

NHTSA also states that novice teen drivers are twice as likely as adult drivers to be in a fatal crash, and that the first months of unsupervised driving are especially risky.[2] That safety risk is one reason young driver coverage can be more expensive.

Less driving history

New drivers have fewer years of safe driving experience for insurers to evaluate.

Higher crash exposure

Inexperience, distractions, passengers, night driving, and speed can increase risk for young drivers.

Discounts may help

Good student, driver education, safe driving, family policy, and telematics programs may lower costs for eligible drivers.

Coverage Options Young Drivers Should Understand

A low monthly premium is helpful, but it should not be the only factor. The Insurance Information Institute explains that auto insurance can include property coverage, liability coverage, and medical coverage, with common policy parts such as liability, collision, comprehensive, medical payments or PIP where applicable, and uninsured or underinsured motorist coverage.[3]

| Coverage Type | What It Generally Does | Why It Matters for Young Drivers |

|---|---|---|

| Liability coverage | Helps pay for injuries or property damage you cause to others, up to policy limits. | Usually required by state law. Minimum limits may not be enough after a serious crash. |

| Collision coverage | Helps repair or replace your own car after a covered crash, subject to the deductible. | Important if the vehicle is financed, leased, newer, or too expensive to replace out of pocket. |

| Comprehensive coverage | Helps with non-collision losses such as theft, vandalism, fire, hail, falling objects, flood, animal damage, or certain glass claims. | Useful for financed, leased, newer, higher-value, or higher-risk vehicles. |

| Uninsured or underinsured motorist coverage | May help when another driver has no insurance or not enough insurance. | Can protect a young driver if another driver cannot fully pay for covered losses. |

| Medical payments or PIP | May help with accident-related medical costs, depending on state and policy terms. | Availability and requirements vary by state, so young drivers should ask how it works locally. |

Discounts are useful, but young drivers should first make sure the policy meets state law, lender requirements, and realistic financial protection needs.

Young Driver Auto Insurance vs. General Auto Insurance

The coverage types are usually the same, but the shopping strategy is different. A young driver may need more attention to discounts, vehicle choice, family policy options, safe driving programs, payment schedules, and whether the policy can stay active without missed payments.

| Shopping Factor | Why It Matters | What to Compare |

|---|---|---|

| Family policy vs. separate policy | III notes that it is generally cheaper to put a teenage driver on the family policy.[4] | Total household premium, assigned vehicle rules, discounts, and liability exposure. |

| Vehicle choice | Repair cost, safety features, theft risk, value, and performance can affect pricing. | Quote insurance before buying or assigning a car to a young driver. |

| Deductible choice | A higher deductible can lower premium but creates a larger claim cost. | Choose a deductible the driver or household could actually pay. |

| Discount eligibility | Discounts vary by insurer and state. | Ask about good student, driver education, safe driver, multi-car, anti-theft, and paperless discounts. |

| Payment schedule | A lower first payment may come with fees, higher later payments, or stricter cancellation rules. | Compare the full six-month or annual cost, not just the first payment. |

Affordable Coverage for Young Drivers

Affordable auto insurance does not always mean the cheapest quote. It means a policy that balances price, legal compliance, claim support, and enough protection for the driver’s real situation. A young driver with an older paid-off car may need a different policy than a student driving a financed vehicle or a teen added to a family policy.

Drivers comparing cheap car insurance for young drivers should review liability limits, deductibles, payment terms, exclusions, optional coverage, and whether the quote includes the protection they actually need.

Before choosing a young driver policy, compare:

- State minimum requirements and whether higher liability limits make sense.

- Collision and comprehensive coverage if the car is financed, leased, newer, or valuable.

- Deductibles and whether the household could afford them after a claim.

- Monthly payment fees, late fees, reinstatement fees, and cancellation rules.

- Good student, driver training, safe driving, anti-theft, paperless, and multi-policy discounts.

- Claim support, policy updates, proof-of-insurance timing, and customer service expectations.

Discounts and Benefits Young Drivers Should Ask About

Not every discount is available in every state or from every insurer, but young drivers should still ask. The Insurance Information Institute says driver education and good student discounts can help reduce the cost of insuring teenage drivers.[5] NAIC also recommends asking about discounts and comparison shopping when trying to save on auto insurance.[6]

| Discount or Strategy | How It May Help | What to Ask |

|---|---|---|

| Good student discount | May lower rates for students who meet academic requirements. | What grade level, documentation, and renewal proof are required? |

| Driver education or defensive driving | May show lower risk and help qualify for savings where available. | Which courses qualify, and does the discount apply to this driver? |

| Family policy | Can sometimes cost less than a separate young driver policy. | How will adding the young driver affect the household premium and coverage? |

| Student away at school | May help if the student lives away from home and does not regularly use the car. | What distance, school status, and vehicle-use rules apply? |

| Telematics or safe driving program | May reward careful driving, lower mileage, or safer habits. | Can the rate go up as well as down, and what data is collected? |

| Vehicle safety or anti-theft features | May reduce risk or qualify for certain discounts. | Which vehicle features does the insurer recognize? |

Safe Driving Can Protect Both Rates and People

Safe driving is not only about insurance savings. NHTSA says novice teen drivers rarely crash while supervised by adults, but have the highest crash rates during the first six months of unsupervised driving after becoming fully licensed.[7]

Habits that can help young drivers

- Avoid phone use and other distractions while driving.

- Follow passenger restrictions and graduated driver licensing rules.

- Drive more cautiously at night, in bad weather, and in heavy traffic.

- Keep a clean driving record by avoiding tickets and at-fault crashes.

- Practice with an experienced adult in different road and weather conditions.

- Review the insurance policy before changing cars, moving, or adding household drivers.

Flexible Payment Options for Young Drivers

Young drivers and families often care about the first payment, monthly payment, and total policy cost. Flexible payment options can help with cash flow, but they should not hide weak coverage, high fees, or strict cancellation terms.

Drivers comparing payment flexibility can review buy now pay later car insurance and cheap car insurance with no deposit to better understand low upfront payment language, installment fees, proof-of-insurance timing, and cancellation risk.

Do not drive until the policy is bound, the required payment is accepted, the policy start date is confirmed, and proof of insurance is issued.

How to Compare Young American Auto Insurance Options

A useful quote comparison uses the same driver, vehicle, garaging ZIP code, coverage limits, deductibles, and optional coverages across every quote. Otherwise, the cheapest quote may simply be offering less protection.

Compare liability limits, collision, comprehensive, UM/UIM, MedPay or PIP, and deductibles before comparing price.

Review the full policy-term premium, installment fees, late fees, and renewal expectations.

Ask which discounts are applied and what proof is required to keep them at renewal.

Understand what happens after a missed payment, failed payment, or coverage lapse.

For a broader overview of liability, comprehensive, collision, deductibles, and policy terms, see our car insurance guide.

Common Mistakes to Avoid

Young drivers can save money, but some shortcuts can create expensive problems later. Before choosing the lowest quote, make sure the coverage actually fits the driver, vehicle, state requirements, and household finances.

| Mistake | Why It Can Hurt | Better Approach |

|---|---|---|

| Choosing minimum limits only | Minimum liability can be too low after a serious crash. | Compare higher liability limits if the household has income, savings, or assets to protect. |

| Dropping physical damage coverage on a financed car | This may violate lender or lease requirements. | Confirm lender requirements before removing collision or comprehensive. |

| Picking a deductible that is too high | The policy may become hard to use after a claim. | Choose a deductible the driver or family could realistically pay. |

| Comparing only monthly price | A low monthly payment may hide fees, low limits, or missing coverage. | Compare the full policy cost and the full coverage package. |

| Ignoring policy start date | A quote is not proof of active insurance. | Wait for policy approval, accepted payment, confirmed start date, and proof of insurance. |

Final Thoughts on Young American Auto Insurance Options

Young drivers can face higher insurance costs, but they are not limited to one option. The better strategy is to compare coverage carefully, ask about discounts, choose a practical vehicle, avoid coverage lapses, drive safely, and review total cost instead of focusing only on the first payment.

The right policy should meet state requirements, protect the vehicle appropriately, fit the deductible budget, and make payment and cancellation rules clear before the driver gets on the road.

Simple rule for young drivers

Choose the lowest-priced policy only after confirming that it meets legal requirements, protects the car appropriately, fits your deductible budget, and does not create a high risk of cancellation.

Compare Young Driver Auto Insurance Before You Buy

The best young driver policy is not always the cheapest. Compare the full cost, coverage limits, deductibles, discounts, and payment rules before choosing a plan.

Frequently Asked Questions

Why is car insurance expensive for young drivers?

Young drivers often pay more because they have less experience and are considered higher risk. Insurance pricing can also depend on vehicle type, ZIP code, driving history, coverage limits, deductibles, and discounts.

What coverage should a young driver carry?

At minimum, a young driver must meet state requirements. Depending on the car, budget, lender rules, and savings, collision, comprehensive, uninsured motorist coverage, and higher liability limits may also be worth comparing.

Can good grades lower auto insurance?

Some insurers offer good student discounts for eligible students. Requirements vary, so students should ask what grade level, documents, and renewal proof are needed.

Is it cheaper for a teen to have a separate policy?

It is often cheaper to add a teen to a family policy than to buy a separate policy, but this depends on the insurer, state, vehicle, household drivers, and coverage limits.

How can young drivers lower their premiums?

Young drivers can compare quotes, keep a clean record, ask about good student and driver education discounts, choose a safe affordable vehicle, consider a family policy, and review deductibles carefully.

Is a quote the same as proof of insurance?

No. A quote is not active coverage. Coverage should be treated as active only after the policy is approved, payment requirements are met, the start date is confirmed, and proof of insurance is issued.

References

- [1] Insurance Information Institute, “Students.” Source ↩

- [2] National Highway Traffic Safety Administration, “Teen Driving.” Source ↩

- [3] Insurance Information Institute, “Auto Insurance Basics: Understanding Your Coverage.” Source ↩

- [4] Insurance Information Institute, “Students.” Source ↩

- [5] Insurance Information Institute, “Students.” Source ↩

- [6] National Association of Insurance Commissioners, “Tips for Saving on Your Auto Insurance.” Source ↩

- [7] National Highway Traffic Safety Administration, “Teen Driving.” Source ↩