By Young Americans Insurance Editorial Team

Published on · Updated on

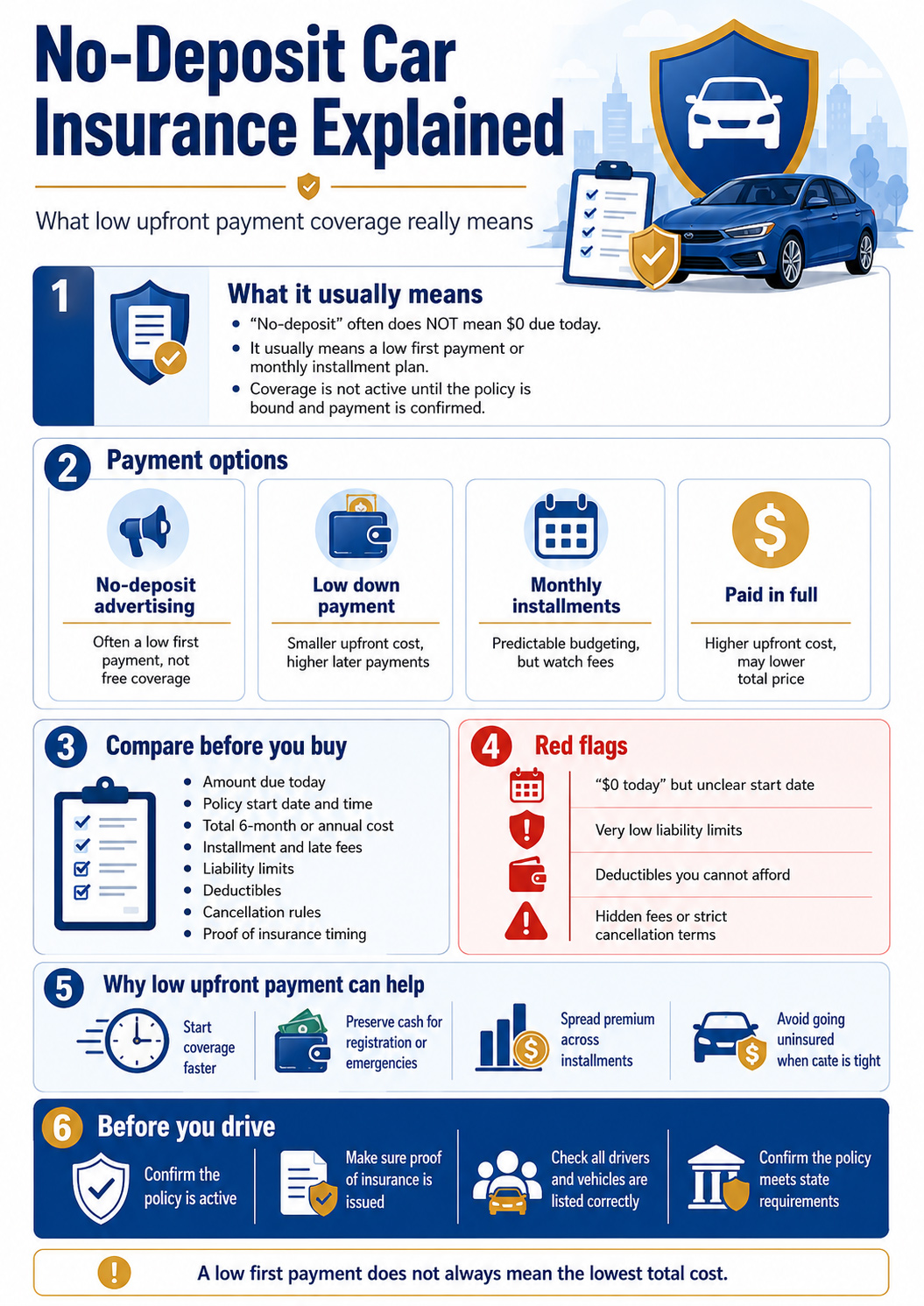

No-deposit car insurance usually does not mean you can start a valid auto policy with nothing due today. In most cases, it means a lower first payment, a monthly installment plan, or no separate deposit beyond the first premium payment.

The safest way to compare no-deposit or low-down-payment car insurance is to check the amount due today, the full policy cost, the coverage limits, the deductible, the payment schedule, and when proof of insurance is issued.

What Does No-Deposit Car Insurance Really Mean?

No-deposit car insurance is often used as marketing language for policies with a lower upfront payment. Most insurers still require some payment before coverage is bound, because a policy generally cannot become active until the first premium payment or another approved billing arrangement is completed.

For drivers who need coverage quickly, the goal should not be only to find the smallest first payment. The goal should be to find a policy that starts on time, provides valid proof of insurance, meets state requirements, and does not become more expensive because of fees or weak coverage.

Low first payment

The first payment may be smaller than a traditional down payment, but later monthly payments may be higher.

Installment plan

The premium may be split into monthly payments, sometimes with billing, service, processing, or installment fees.

Active coverage matters

A quote is not proof of insurance. Coverage should be confirmed before driving.

A quote, estimate, or online form does not mean coverage is active. Wait until the policy is bound, the start date is confirmed, and proof of insurance is available.

No Deposit vs. Low Down Payment vs. Paid in Full

Drivers often compare no-deposit policies against low-down-payment policies and paid-in-full policies. Each option can work, but the best choice depends on cash flow, total cost, cancellation risk, and how reliably you can keep payments current.

| Payment Option | How It Usually Works | Best For | What to Watch |

|---|---|---|---|

| No-deposit advertising | Often means a very low first payment or no separate deposit, not necessarily $0 due. | Drivers comparing urgent coverage with limited cash available. | Confirm the exact binding payment, fees, and whether coverage starts immediately. |

| Low down payment | You pay a smaller amount upfront, then the remaining premium is divided into installments. | Drivers who need coverage now but want to preserve cash. | Later payments may be higher, and total cost may exceed paid-in-full pricing. |

| Monthly installments | The policy premium is spread over monthly payments. | Drivers who prefer predictable monthly budgeting. | Installment fees, late fees, and cancellation after missed payments. |

| Paid in full | The full premium is paid at the start of the policy term. | Drivers who can afford the upfront cost and want fewer billing problems. | Higher upfront cost, but it may reduce fees or qualify for a discount. |

How to Compare No-Deposit Car Insurance Quotes

The best no-deposit car insurance quote is not always the quote with the lowest first payment. The National Association of Insurance Commissioners recommends comparing coverage, deductibles, discounts, and total premium when shopping for auto insurance.[1]

Before choosing a quote, compare:

- The amount due today to start coverage.

- The exact policy start date and time.

- The total six-month or annual policy cost.

- Monthly billing, installment, processing, or late fees.

- Liability limits and whether they are only state minimums.

- Deductibles for collision and comprehensive coverage.

- Cancellation rules if a payment is missed.

- Discounts for safe driving, bundling, student status, telematics, or low mileage.

Coverage Trade-Offs to Review Carefully

A policy with a very low first payment can still be risky if it comes with weak coverage, high deductibles, or strict cancellation terms. The Insurance Information Institute explains that liability insurance pays for damage you cause to others, while optional collision and comprehensive coverages can help pay for damage to your own car.[2]

| Coverage Choice | How It Affects Price | Risk to Consider |

|---|---|---|

| State-minimum liability only | Often cheaper than higher limits or broader coverage. | May not provide enough protection after a serious accident. |

| Higher deductibles | Can reduce premiums for collision or comprehensive coverage. | You must be able to pay the deductible after a claim. |

| Dropping collision | May lower the premium on an older paid-off vehicle. | Your own car may not be covered after an at-fault crash. |

| Dropping comprehensive | May lower cost if the vehicle has low value. | Theft, vandalism, hail, fire, or falling object damage may not be covered. |

| Reducing optional protection | May lower the monthly price. | Can leave you with larger out-of-pocket costs after a loss. |

The cheapest first payment may not be the cheapest policy. Always compare the total cost and the coverage you are giving up.

No-Deposit Car Insurance Red Flags

Some low-upfront-payment offers are useful, but others can be misleading. Before entering payment information, review the offer carefully and confirm that the insurer or agency is licensed to sell coverage in your state.

Do not drive unless the policy is active and proof of insurance has been issued.

State minimum coverage may be legal, but it may not fully protect you after a serious accident.

A high deductible can reduce the premium but create a financial problem after a claim.

Installment fees, late fees, and short cancellation windows can make the policy harder to keep active.

Payment Plans, Late Fees, and Lapse Risk

Flexible payment plans can help drivers manage cash flow, but missed payments can create problems. The Consumer Financial Protection Bureau explains that many buy now, pay later arrangements may charge late fees if payments are not made on time. For insurance, missed premium payments can also lead to policy cancellation under the policy terms and state rules.[3]

Before accepting a low-first-payment policy, ask when each installment is due, how much each payment will be, whether autopay is required, what late fees apply, and how quickly the policy can cancel after nonpayment.

When Low Upfront Payments Can Help

No-deposit or low-upfront-payment insurance can be helpful when a driver needs coverage quickly and cannot comfortably pay a large premium all at once. It may be useful after buying a car, moving to a new state, adding a household driver, recovering from a lapse, or replacing a canceled policy.

Potential benefits include:

- Starting required coverage with less money due upfront.

- Keeping more cash available for registration, repairs, fuel, or emergency expenses.

- Spreading the premium across monthly payments.

- Making it easier to compare several insurers instead of choosing the first offer.

- Helping drivers avoid going uninsured when they need coverage immediately.

When Paying More Upfront May Be Better

A lower first payment is not always the best deal. Paying more upfront, or paying in full, may reduce billing fees, lower the chance of missing an installment, and sometimes qualify for a discount. NAIC’s auto insurance shopping guidance reminds consumers to compare discounts, deductibles, limits, optional coverage, and total premium instead of focusing on one number.[4]

| Question | Why It Matters |

|---|---|

| How much is due today? | This determines whether the policy is realistic for your current budget. |

| How much is due each month? | A low first payment can lead to higher later installments. |

| What is the total policy cost? | The lowest initial payment may not be the lowest total price. |

| Are there installment or service fees? | Fees can make monthly payments more expensive over time. |

| Can you keep every payment current? | Missed payments can cause cancellation and lapse risk. |

Legal Requirements and Compliance

Every state has its own auto insurance or financial responsibility rules. A no-deposit policy is only useful if it satisfies the state’s legal requirements and any lender or lease obligations. If a driver is caught without required insurance, the consequences may include fines, license suspension, registration problems, reinstatement fees, or higher future premiums.

Before buying, make sure the policy provides valid proof of insurance and meets the rules in the state where the vehicle is registered. If you need an SR-22, FR-44, or another financial responsibility filing, confirm that the insurer can file it before paying.

Compliance checklist

- Confirm the insurer or agency is licensed in your state.

- Confirm the policy meets your state’s minimum coverage requirements.

- Confirm whether the vehicle is financed or leased and whether the lender requires collision and comprehensive coverage.

- Confirm all household drivers who should be listed are included.

- Confirm proof of insurance will be available before you drive.

Before You Buy: No-Deposit Car Insurance Checklist

Use this checklist before choosing a no-deposit, low-down-payment, or monthly installment policy. The goal is to avoid weak coverage, surprise fees, or a payment schedule that creates lapse risk.

Before paying, confirm:

- The exact amount due today.

- The exact policy start date and time.

- When proof of insurance will be issued.

- The full six-month or annual premium.

- The monthly payment schedule.

- Any installment, service, processing, or late fees.

- The cancellation rule after missed payments.

- Liability limits, deductibles, and optional coverages.

- Whether collision and comprehensive are required by a lender or lease.

- Whether all regular drivers and vehicles are listed correctly.

Frequently Asked Questions

Is no-deposit car insurance real?

It can be, but the phrase is often misleading. Many “no deposit” offers still require a first payment, policy fee, or approved billing arrangement before coverage starts.

Can I drive before making the first payment?

No. You should not drive until the policy is active and you have proof of insurance. A quote alone is not coverage.

Is no-deposit insurance cheaper?

Not always. It may lower the amount due today, but monthly fees or higher later payments can make the total policy cost higher than a paid-in-full option.

What should I compare besides the first payment?

Compare liability limits, deductibles, collision and comprehensive coverage, uninsured motorist coverage, discounts, total premium, installment fees, and cancellation rules.

Can missed payments cancel my policy?

Yes. If required payments are missed, the insurer may cancel the policy according to state law and policy terms. A lapse can create legal and financial problems.

Should I choose liability-only coverage to lower my payment?

Liability-only coverage can reduce the price, but it may not repair your own vehicle after an at-fault crash, theft, vandalism, hail, fire, or other covered physical damage loss. Compare the savings against the risk.

Final Thoughts on No-Deposit Car Insurance

No-deposit car insurance can help drivers who need a lower first payment, but it should not be confused with free coverage or permission to drive before a policy is active. The most important details are the start date, proof of insurance, total premium, payment schedule, coverage limits, deductibles, and cancellation rules.

The best policy is not always the one with the smallest first payment. Compare the full cost and the protection you are buying before choosing a no-deposit or low-down-payment plan.

Compare Low Down Payment Car Insurance Carefully

Look beyond the first payment. Compare the total premium, coverage limits, deductibles, discounts, fees, and cancellation rules before choosing a no-deposit or low-down-payment policy.

Compare Auto Insurance OptionsReferences

- National Association of Insurance Commissioners, Tips for Saving on Your Auto Insurance. Source ↩

- Insurance Information Institute, Auto Insurance Basics: Understanding Your Coverage. Source ↩

- Consumer Financial Protection Bureau, Do Buy Now, Pay Later Loans Have Fees? Source ↩

- National Association of Insurance Commissioners, Best Practices for Buying Auto Insurance. Source ↩