By Young Americans Insurance Editorial Team

Published on · Updated on

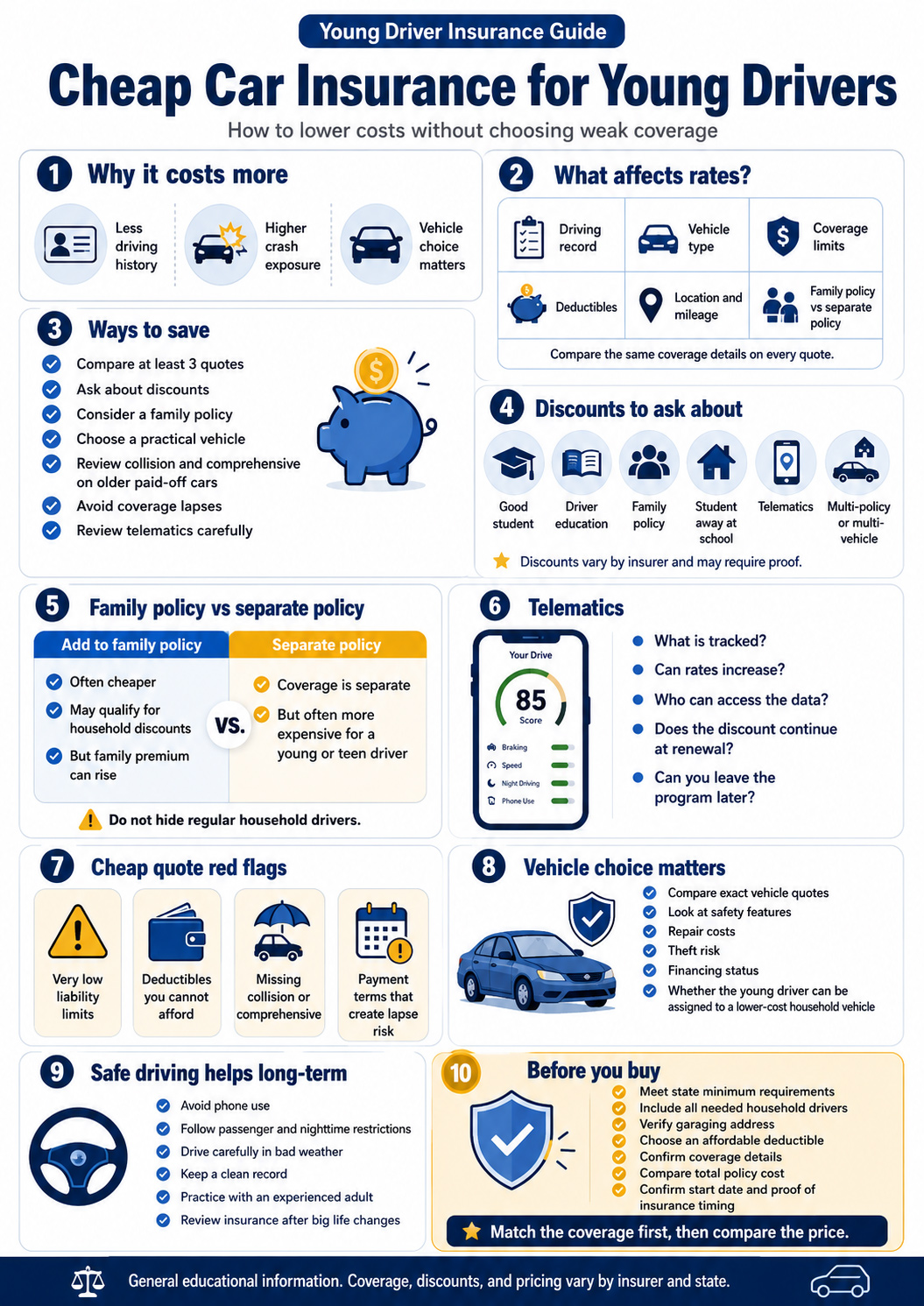

Cheap car insurance for young drivers is possible, but the cheapest monthly payment is not always the safest choice. Young drivers, parents, and students should compare coverage limits, deductibles, discounts, vehicle choice, telematics options, and family policy strategies before choosing a policy.

In this guide, “young drivers” can include teen drivers, newly licensed drivers, college students, and drivers under 25 with limited insurance history. The right policy should meet state requirements, protect against major financial risk, and avoid coverage gaps that can make future insurance more expensive.

Why Car Insurance Costs More for Young Drivers

Young drivers often pay higher premiums because insurers price policies based on risk. The Insurance Information Institute describes teenage drivers as one of the highest-risk segments and says they can add 50% to 100% to the cost of a family auto policy.[1]

NHTSA also says novice teen drivers are twice as likely as adult drivers to be in a fatal crash. That does not mean every young driver is unsafe, but it helps explain why insurers often charge more until a driver builds experience and a cleaner record.[2]

Young drivers can still improve their options by comparing quotes, asking about discounts, choosing a safer vehicle, avoiding distracted driving, and keeping coverage active without lapses.

Less driving history

Insurers have less data to judge risk, so new drivers may be priced more cautiously.

Higher crash exposure

Inexperience, passengers, distractions, night driving, and speed can all affect young driver risk.

Vehicle choice matters

Safer, practical vehicles often cost less to insure than high-performance or expensive-to-repair cars.

What Affects Young Driver Insurance Rates?

Auto insurance pricing can depend on many factors. The Insurance Information Institute lists items such as driving record, vehicle use, location, age, gender, vehicle type, coverage choices, deductibles, and credit-based insurance score where allowed by state law.[3]

| Rating Factor | Why It Matters | What Young Drivers Can Do |

|---|---|---|

| Driving record | Tickets, at-fault crashes, and claims can increase premiums. | Drive safely, avoid distractions, and follow state graduated licensing rules. |

| Vehicle type | Repair cost, safety features, theft risk, and vehicle value can affect insurance cost. | Compare insurance costs before buying a car. |

| Coverage limits | Higher liability limits and optional coverage can cost more but provide stronger protection. | Compare the same limits across every quote. |

| Deductibles | Higher deductibles may reduce premium but increase out-of-pocket claim cost. | Choose a deductible you can actually afford after a loss. |

| Location and mileage | ZIP code, traffic, theft risk, and annual mileage can affect pricing. | Report garaging address and mileage accurately. |

| Family policy vs. separate policy | Teen drivers are often cheaper to add to a family policy than to insure separately. | Compare both options before deciding. |

Young Driver vs. Teen Driver vs. College Student

Not every young driver has the same insurance situation. A 16-year-old newly licensed driver, a 20-year-old college student, and a 24-year-old with several clean years of driving history may receive very different quotes.

| Driver Situation | Common Insurance Issue | Useful Strategy |

|---|---|---|

| Teen driver | Limited driving history and higher risk pricing. | Compare family policy pricing, good student discounts, driver education, and a safer vehicle assignment. |

| Newly licensed young adult | No prior insurance history or limited continuous coverage. | Compare multiple quotes, avoid lapses, and ask how rates may change after a clean renewal period. |

| College student | Vehicle may be at school, at home, or used only during breaks. | Ask about student-away-at-school discounts and make sure the garaging address is accurate. |

| Young driver buying a first car | Vehicle choice can raise or lower the total insurance cost. | Compare insurance costs before buying the car, especially for collision and comprehensive coverage. |

Tips for Finding Affordable Car Insurance for Young Drivers

The best strategy is to lower risk without weakening coverage too much. A quote may look cheap because it has state-minimum liability, high deductibles, no collision or comprehensive coverage, or strict payment rules. Compare the full policy before choosing.

Young driver savings checklist

- Compare at least three quotes using the same liability limits and deductibles.

- Ask about good student, driver education, defensive driving, and safe driver discounts.

- Consider staying on a family policy if it is cheaper and allowed.

- Choose a practical vehicle with good safety features and reasonable repair costs.

- Review collision and comprehensive coverage if the car is older and fully paid off.

- Set payment reminders to avoid a lapse in coverage.

- Ask whether telematics can lower the rate, and review the privacy terms before enrolling.

The cheapest policy is not always the safest choice if it leaves the driver with low liability limits, unaffordable deductibles, or missing coverage. NAIC says drivers may reduce costs by raising deductibles on collision and comprehensive coverage, but they should first make sure they can afford the higher out-of-pocket amount after an accident.[4]

Discounts Young Drivers Should Ask About

Discounts vary by state and insurer, but young drivers should ask about every available option. Some discounts require proof, such as report cards, course completion certificates, enrollment documents, or participation in a driving program.

| Discount or Strategy | How It May Help | What to Ask |

|---|---|---|

| Good student discount | May reduce premiums for eligible students who meet grade requirements. | What GPA, age, enrollment status, or documents are required? |

| Driver education discount | May help if the driver completes an approved course. | Which courses qualify in my state? |

| Family policy | Often cheaper than a separate policy for a teen driver. | How much will the family premium increase? |

| Student away at school | May help if the student lives away from home and does not regularly drive the car. | How far away must the student be, and can the car stay at home? |

| Telematics or usage-based insurance | May reward safer driving or lower mileage. | Can the rate increase as well as decrease? What data is collected? |

| Multi-policy or multi-vehicle | May reduce the total household insurance cost. | Is bundling actually cheaper than separate policies? |

Family Policy vs. Separate Policy for Young Drivers

For many teen drivers, being added to a family policy is cheaper than buying a separate policy. The Insurance Information Institute says it is generally cheaper to put a teenage driver on the family policy, and driver education or good student discounts may reduce the impact.[5]

| Option | Potential Advantage | Potential Drawback |

|---|---|---|

| Add to family policy | May be cheaper and may qualify for household discounts. | The overall family premium can increase significantly. |

| Separate policy | Can keep the young driver’s coverage separate from the household policy. | Often more expensive for a teen or new driver. |

| Assign driver to a specific car | Can help match the young driver with a safer, cheaper-to-insure vehicle. | Rules vary by insurer and household vehicle use. |

| Student away at school | May reduce cost if the student does not regularly drive the car. | Eligibility depends on distance, school status, and insurer rules. |

Do not hide a young driver who regularly uses a household vehicle. Undisclosed drivers can create claim problems, cancellation risk, or premium adjustments. Ask the insurer how household drivers should be listed.

Telematics and Usage-Based Insurance

Telematics can be useful for careful young drivers who want a chance to prove safer habits. NAIC explains that usage-based auto insurance tracks mileage and driving behaviors, often through vehicle technology, a plug-in device, or a mobile app.[6]

Programs vary. Some may look at mileage, braking, acceleration, speed, time of day, phone use, or other driving behaviors. They may offer savings for safer driving, but drivers should read the privacy terms and confirm whether poor scores can raise the rate.

Before enrolling in telematics, ask:

- What driving behaviors are tracked?

- Can my premium increase if my score is poor?

- Who can access the data?

- How long is the monitoring period?

- Does the discount continue at renewal?

- Can I leave the program later?

- Does the program track phone use, location, time of day, or hard braking?

Cheap Quote Red Flags for Young Drivers

A low quote can be useful, but it can also hide weak protection. Before choosing the cheapest option, look for the details that often make a quote cheaper on paper but riskier in real life.

State minimum liability may satisfy the law, but it may not fully protect a household after a serious accident.

A higher deductible may lower the premium, but it can create a problem if the young driver has a claim.

Liability-only coverage may not repair the young driver’s own vehicle after a crash, theft, hail, fire, or vandalism.

Strict billing rules, high fees, or missed reminders can cause cancellation and make future insurance harder to afford.

Vehicle Choice Can Make Young Driver Insurance Cheaper

The car matters. A young driver with a practical, safe, lower-cost vehicle may receive better quotes than a young driver with a high-performance, luxury, modified, or expensive-to-repair vehicle. Insurers may consider repair costs, theft risk, safety features, vehicle value, and how often similar vehicles are involved in claims.

Before buying a car for a young driver, compare:

- Insurance quote for the exact year, make, model, and trim.

- Collision and comprehensive cost with realistic deductibles.

- Safety features and crash-avoidance technology.

- Repair cost, parts availability, and theft risk.

- Whether the car will be financed, leased, or paid off.

- Whether the young driver can be assigned to a lower-cost household vehicle.

For more vehicle-specific planning, review cars that may be cheaper to insure for teens before choosing a vehicle.

Safe Driving Is Still the Biggest Long-Term Strategy

Discounts and quote comparison help, but safe driving is the most important long-term strategy. NHTSA emphasizes that teen driving risk is affected by factors such as inexperience, passengers, distraction, speeding, and nighttime driving.[7]

Habits that can help protect rates and safety

- Avoid phone use while driving.

- Follow passenger and nighttime driving restrictions.

- Drive more carefully in rain, snow, traffic, or unfamiliar areas.

- Keep a clean record by avoiding speeding tickets and at-fault crashes.

- Practice with an experienced adult in different road conditions.

- Review insurance before changing vehicles, moving, or adding a driver.

How to Compare Quotes Without Getting Misled

The cheapest quote may have weaker limits, fewer coverages, higher deductibles, or more restrictive payment terms. Young drivers and parents should compare the full policy, not just the first payment or monthly price.

Simple comparison rule

Use the same drivers, same vehicle, same liability limits, same deductible, same optional coverages, and same payment schedule when comparing quotes.

Before buying, confirm:

- The policy meets your state’s minimum insurance requirements.

- All household drivers who should be listed are included.

- The vehicle garaging address is accurate.

- The deductible is affordable after a claim.

- The quote includes the coverages you actually want.

- The total policy cost is clear, including fees and installment charges.

- The policy start date and proof of insurance timing are confirmed.

Drivers researching auto insurance options for young drivers should also check company licensing, claims support, cancellation rules, and payment fees before buying.

Frequently Asked Questions

Why is car insurance expensive for young drivers?

Young drivers often pay more because insurers consider them higher risk. Teenage drivers have less driving history and are statistically more likely to be involved in serious crashes than more experienced adult drivers.

Is it cheaper to add a teen driver to a family policy?

Often, yes. The Insurance Information Institute says it is generally cheaper to put a teenage driver on the family policy rather than buying a separate policy.

What discounts should young drivers ask about?

Young drivers should ask about good student, driver education, defensive driving, safe driver, telematics, student away at school, multi-vehicle, and multi-policy discounts.

Can telematics lower young driver insurance costs?

It can for some drivers. Usage-based insurance may track mileage and driving behavior. Before enrolling, ask what data is collected, whether the rate can increase, and whether the discount continues at renewal.

What is the best car for cheap young driver insurance?

There is no single best car, but practical vehicles with good safety features, reasonable repair costs, and lower theft risk may be cheaper to insure than sports cars, luxury vehicles, or expensive-to-repair models.

Should young drivers choose the cheapest liability-only policy?

Not automatically. Liability-only coverage may be cheaper, but it may not repair the young driver’s own vehicle after an at-fault crash or many non-collision losses. Compare the savings against the risk before removing coverage.

How can a young driver lower rates over time?

Keeping a clean driving record, avoiding coverage lapses, choosing a practical vehicle, maintaining good grades if eligible, and comparing quotes at renewal can help improve affordability over time.

Final Thoughts on Cheap Car Insurance for Young Drivers

Cheap car insurance for young drivers should not mean weak protection. The best policy is usually the one that balances affordable price, required liability coverage, realistic deductibles, useful discounts, safe vehicle choice, and stable payment terms.

Parents and young drivers should compare quotes carefully, avoid hiding household drivers, ask about every discount, and build a clean driving record. A slightly higher premium can be worth it if it prevents major financial exposure after an accident or lapse.

Compare Young Driver Car Insurance Carefully

The right young driver policy should be affordable, but it should also meet state requirements, protect the vehicle appropriately, include useful discounts, and avoid coverage gaps.

Compare Auto Insurance OptionsReferences

- Insurance Information Institute, Students. Source ↩

- National Highway Traffic Safety Administration, Teen Driving. Source ↩

- Insurance Information Institute, What Determines the Price of an Auto Insurance Policy? Source ↩

- National Association of Insurance Commissioners, Tips for Saving on Your Auto Insurance. Source ↩

- Insurance Information Institute, Students. Source ↩

- National Association of Insurance Commissioners, Telematics. Source ↩

- National Highway Traffic Safety Administration, Teen Driving. Source ↩