By Young Americans Insurance Editorial Team

Created on · Updated on

Reviewed for insurance topic clarity, source quality, quote-comparison usefulness, and YMYL/consumer disclosure standards.

Insurance for young adults should start with the risks that affect daily life first: driving, renting, medical coverage, emergency costs, and whether anyone depends on your income. The goal is not to buy every policy available, but to understand which coverage fits your car, apartment, budget, family situation, and stage of life.

This guide focuses on practical first policies for young adults, especially auto insurance and renters insurance, while also explaining when health coverage and life insurance may need attention.

Why Insurance Matters for Young Adults

Young adults often face several financial transitions at the same time: moving away from home, driving more often, signing a lease, starting a job, managing school costs, or becoming responsible for their own bills. Insurance can help reduce the financial shock of a covered accident, theft, lawsuit, medical event, or property loss.

The most useful insurance plan is not always the cheapest one. A low monthly payment may come with weak limits, high deductibles, missing coverage, or fees that make the policy more expensive over time. Young adults should compare the full policy, not only the first price shown.

Protect your transportation

Auto insurance can help keep a covered accident, theft, or liability claim from becoming a major financial setback.

Protect your belongings

Renters insurance can help protect personal property and liability exposure when a landlord’s policy does not cover your belongings.

Protect your budget

Health coverage, deductibles, emergency savings, and careful policy choices can reduce the risk of bills you cannot easily pay.

Which Insurance Should Young Adults Consider First?

Not every young adult needs every type of policy right away. A college student living with family has different needs than a young driver with a financed car, a renter with expensive electronics, or a new parent with someone depending on their income.

| Your Situation | Coverage to Review First | Why It Matters |

|---|---|---|

| You drive regularly | Auto insurance | Most states require auto insurance or financial responsibility. Coverage can also protect against liability, vehicle damage, theft, weather losses, and uninsured drivers depending on the policy. |

| You rent an apartment, room, or student housing | Renters insurance | A landlord’s insurance usually protects the building, not your belongings. A renters policy may also include liability and additional living expense coverage. |

| You are under 26 and comparing health plans | Health coverage | If a parent’s health plan covers dependents, HealthCare.gov says you can usually be added to or stay on that plan until you turn 26. |

| Someone depends on your income | Life insurance | Life insurance may matter if you have children, a spouse, shared debts, co-signed obligations, or family members who would be affected financially. |

| You have a tight monthly budget | Deductibles and payment terms | A low premium can still be risky if the deductible is too high or missed payments could cause a lapse. |

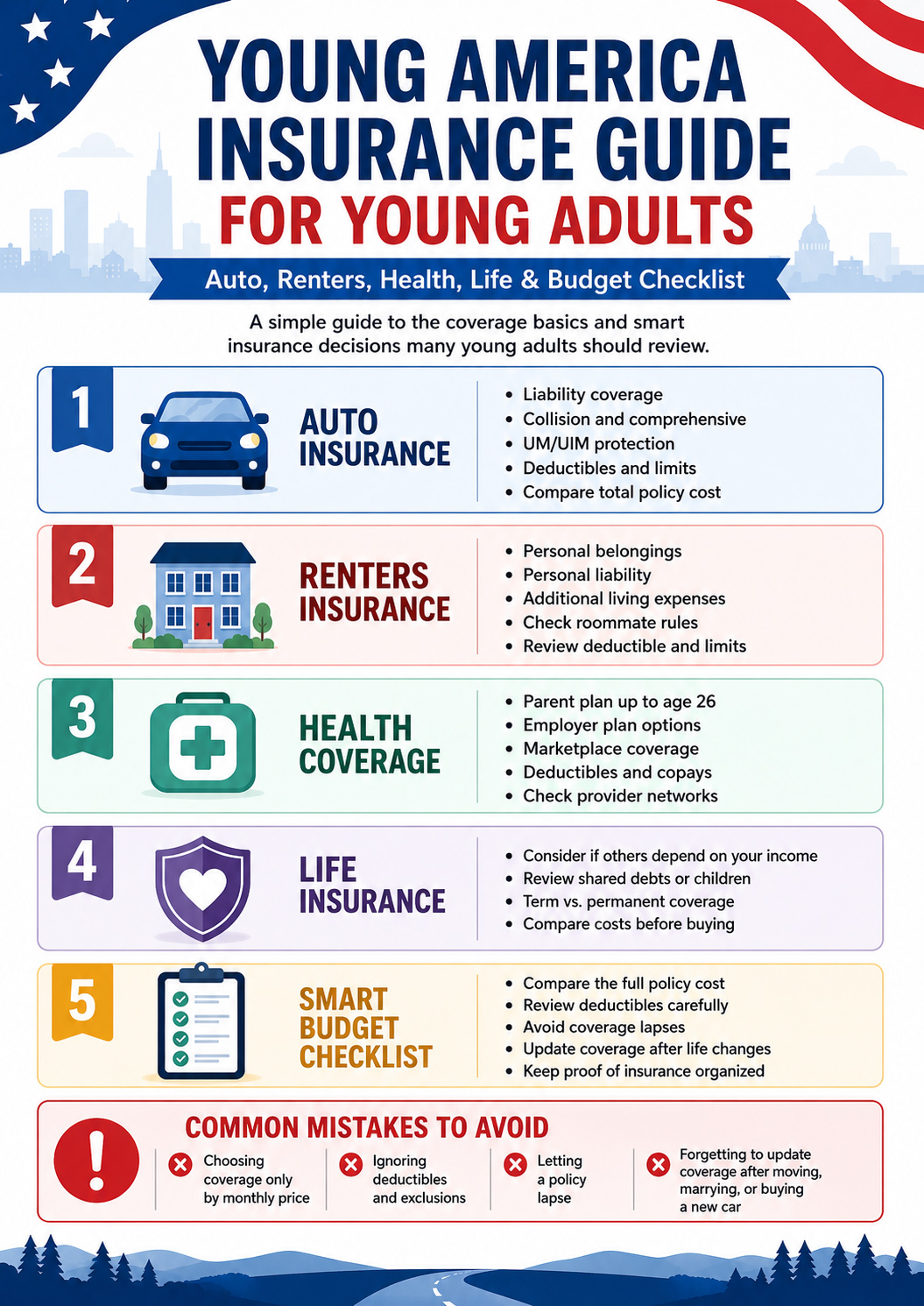

Auto Insurance: The First Policy Many Young Adults Need

For many young adults, driving is connected to work, school, family responsibilities, and independence. Auto insurance should be chosen carefully because a cheap policy may still leave you exposed if liability limits are too low or if your own car is not protected after a covered physical damage loss.

The NAIC explains that auto insurance can include liability, property damage, rental car-related questions, deductibles, uninsured motorist coverage, and other policy details that affect how protection works. That is why young drivers should compare coverage and policy terms, not just the monthly price.[1]

Two policies can look similar but provide very different protection. Compare liability limits, collision, comprehensive, uninsured motorist coverage, deductibles, rental reimbursement, roadside assistance, discounts, fees, and cancellation rules.

| Auto Coverage Area | What It Generally Does | Why Young Adults Should Check It |

|---|---|---|

| Liability coverage | Helps pay for injuries or property damage you cause to others, up to your limits. | Low limits may satisfy state law but may not be enough after a serious accident. |

| Collision coverage | Helps repair or replace your car after a covered crash, usually after a deductible. | Often important if the car is financed, leased, newer, or hard to replace. |

| Comprehensive coverage | Helps with certain non-collision losses such as theft, vandalism, fire, hail, falling objects, or animal damage. | Useful when replacing the car out of pocket would be difficult. |

| Uninsured or underinsured motorist coverage | May help if another driver has no insurance or not enough insurance, depending on state and policy terms. | Can add protection when another driver cannot fully pay for covered losses. |

| Deductibles | The amount you pay out of pocket before certain coverage pays. | A higher deductible may lower premium, but it can create a cash-flow problem after a claim. |

If auto coverage is your first priority, review our car insurance guide, cheap car insurance for young drivers, and young driver quote comparison guide.

Renters Insurance: Small Policy, Important Protection

Many young adults rent apartments, rooms, shared houses, or student housing. The Insurance Information Institute explains that standard renters insurance protects personal belongings against listed events such as fire, smoke, lightning, vandalism, theft, explosion, windstorm, and certain water damage, while floods and earthquakes are not covered by standard renters insurance and may require separate coverage.[2]

Renters insurance checklist

- Estimate the value of electronics, furniture, clothes, shoes, school items, bikes, and personal belongings.

- Ask whether the policy pays replacement cost or actual cash value.

- Review liability limits if you host guests, have pets, or share housing.

- Check whether roommates are covered or need separate policies.

- Review exclusions for flood, earthquake, pests, high-value items, and business property.

- Ask whether additional living expenses are covered if a covered loss makes the rental temporarily unlivable.

For a deeper look at this topic, read our guide to cheap renters insurance for young adults.

Health Coverage: Keep This Section Practical

Health coverage is important because medical care can be expensive. For many young adults, the first question is whether they can stay on a parent’s plan, use an employer plan, choose a student plan, apply through the marketplace, or qualify for another program.

HealthCare.gov states that if a parent’s health insurance plan covers dependents, young adults can usually be added to or stay on that plan until they turn 26.[3] Before choosing a plan, compare the premium, deductible, out-of-pocket maximum, provider network, prescription coverage, emergency care rules, and whether the plan works where you live or study.

If you are under 26

Compare the parent plan against school, employer, marketplace, or other available options. The cheapest monthly premium is not always the best fit if the network or deductible does not work for your needs.

If you are turning 26

Start comparing options before coverage ends. Review employer coverage, marketplace plans, Medicaid eligibility, student plans, and special enrollment rules if applicable.

This article gives general insurance education only. Health plan eligibility, subsidies, networks, and plan rules vary. Review official plan documents and use official marketplace, employer, or insurer resources before choosing coverage.

Life Insurance: When It May Matter

Not every young adult needs a large life insurance policy. It may become more relevant if someone depends on your income, you have children, you share debts, you co-signed obligations, or you want to leave money for final expenses or family support.

The NAIC explains that there are two basic types of life insurance: term insurance and permanent insurance. Term insurance generally provides coverage for a set period, while permanent insurance can provide longer-lasting coverage and may include cash value features.[4]

Term life insurance

Often considered when protection is needed for a specific period, such as years when children are young, debts are being paid, or income replacement is important.

Permanent life insurance

Can be more complex and may include cash value. Compare long-term affordability, fees, surrender rules, guarantees, and whether the policy fits your real need.

How to Avoid Common Insurance Mistakes

Insurance only works if the policy matches the risk and stays active. A policy with a low first payment can still become a problem if later installments are too high, fees add up, or a missed payment causes a lapse.

| Mistake | Why It Can Hurt | Better Approach |

|---|---|---|

| Choosing only the lowest monthly premium | The policy may have weak limits, high deductibles, missing coverage, or strict payment terms. | Compare the total policy cost, coverage limits, deductibles, fees, and exclusions. |

| Ignoring the deductible | A deductible that is too high can make a claim hard to afford. | Choose a deductible that fits your emergency savings and risk tolerance. |

| Letting coverage lapse | A lapse can create legal, financial, or underwriting problems, especially for auto insurance. | Set reminders, use autopay carefully, and contact the insurer before missing a payment. |

| Not updating coverage after life changes | Moving, buying a car, signing a lease, changing jobs, or adding a dependent can change coverage needs. | Review policies at least once a year and after major life events. |

| Assuming every policy covers every loss | Exclusions, sublimits, waiting periods, and claim conditions can limit payment. | Read the declarations page, exclusions, endorsements, and claim rules before buying. |

Budgeting for Insurance Without Overpaying

Insurance should fit your monthly budget, but the lowest price is not always the safest choice. The CFPB’s financial empowerment materials explain that cash-flow budgeting starts with tracking what you earn and spend, analyzing spending, and using that information to set realistic targets for future income and expenses.[5]

Simple budget review

- List fixed expenses such as rent, car payment, phone, student costs, and insurance.

- Separate the first payment from the total six-month or annual policy cost.

- Check installment fees, service fees, late fees, and cancellation rules.

- Keep emergency savings in mind before choosing a high deductible.

- Review whether bundling renters and auto insurance truly lowers the total cost.

- Compare quotes again after moving, buying a car, improving your driving record, or changing household status.

How to Customize Coverage Without Overbuying

Customization does not mean buying every optional add-on. It means matching coverage to your real risk, income, vehicle, housing situation, dependents, and savings. A young adult with a financed car may need collision and comprehensive coverage, while someone with an older paid-off car may compare whether those coverages still make sense.

Check what is legally required, lender-required, lease-required, or contractually required before removing coverage.

Prioritize risks that could create bills you cannot comfortably pay from savings.

Do not choose a high deductible only to lower the premium if you could not pay it after a claim.

Update coverage after moving, changing jobs, buying a car, signing a lease, or adding financial responsibilities.

Simple insurance review formula

Start with required coverage, add protection for losses you cannot afford, avoid unnecessary extras, and revisit your plan when your life changes.

Helpful Young Americans Insurance Resources

These pages can help young adults keep researching before choosing a policy or requesting a quote.

Auto insurance basics

Review common coverage types, policy terms, deductibles, and quote-comparison steps.

Young driver savings

Learn how young drivers can compare policies, discounts, vehicle choices, family policies, and telematics options.

Renters insurance

Understand how renters coverage can protect belongings, liability exposure, and additional living expenses.

Frequently Asked Questions

What insurance should young adults consider first?

Start with coverage tied to immediate risks and requirements: auto insurance if you drive, renters insurance if you rent, health coverage for medical costs, and life insurance if someone depends on your income.

Can young adults stay on a parent’s health insurance plan?

In many cases, yes. HealthCare.gov says that if a parent’s plan covers dependents, young adults can usually be added to or stay on that plan until they turn 26.[3]

Is renters insurance worth it for students or first-time renters?

Often, yes. Renters insurance can help protect personal belongings and may include liability and additional living expense coverage after covered events. Check policy limits, deductibles, exclusions, and roommate rules before buying.

Should young adults buy life insurance?

Life insurance may be worth considering if someone depends on your income, you have children, you share debts, or you want financial protection for beneficiaries. If no one depends on you financially, a large policy may not be necessary right away.

How often should young adults review insurance coverage?

Review coverage at least once a year and after major life changes such as moving, buying a car, signing a lease, changing jobs, getting married, having a child, or taking on new debt.

Final Thoughts on Insurance for Young Adults

Young adults do not need to buy every insurance product at once. The better approach is to identify the biggest financial risks in your current life, meet legal or contract requirements, compare policies carefully, and avoid choosing coverage based only on the lowest monthly payment.

For many young adults, the first priorities are auto insurance, renters insurance, health coverage, and a realistic budget for premiums and deductibles. Life insurance may become more important when dependents, shared debts, or long-term family responsibilities enter the picture.

Compare Auto Insurance Options Before You Need Them

Enter your ZIP code to continue comparing auto insurance options and review quote paths that may fit your coverage needs and budget.

References

- [1] National Association of Insurance Commissioners, “Auto Insurance.” Source ↩

- [2] Insurance Information Institute, “Renters Insurance.” Source ↩

- [3] HealthCare.gov, “How to get or stay on a parent’s plan.” Source ↩

- [4] National Association of Insurance Commissioners, “Life Insurance.” Source ↩

- [5] Consumer Financial Protection Bureau, “Your Money, Your Goals: A Financial Empowerment Toolkit.” Source ↩