By YoungAmericansInsurance.com Editorial Team

Created on · Updated on

Editorial note

The YoungAmericansInsurance.com Editorial Team creates plain-language insurance content for drivers, homeowners, students, and young adults who want to compare coverage options more confidently.

This article is for general informational purposes only and does not replace advice from a licensed insurance professional. Coverage, discounts, eligibility, and pricing vary by insurer, state, vehicle, driver profile, and policy terms.

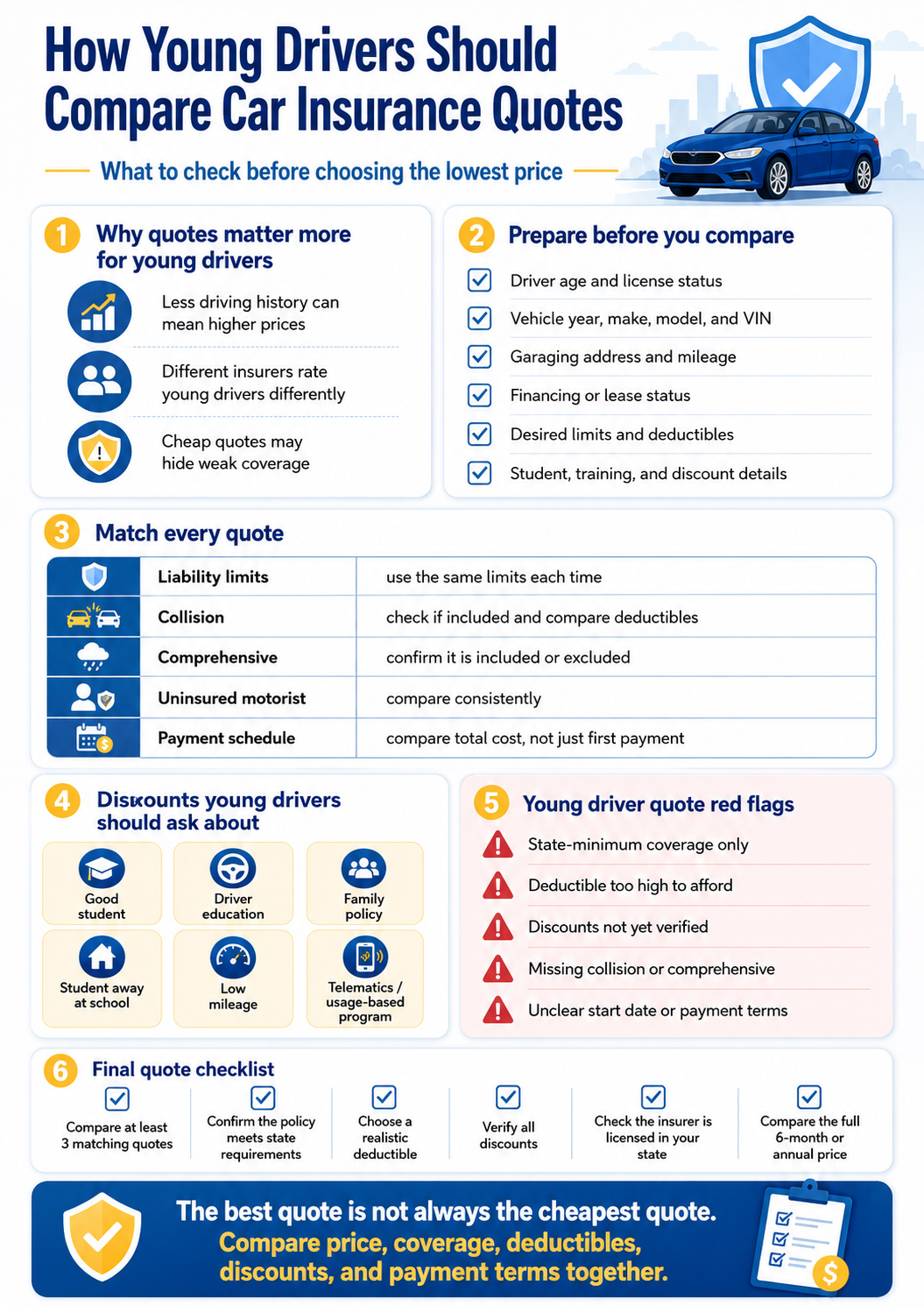

Young drivers should compare car insurance quotes carefully because the lowest monthly price can hide weak liability limits, high deductibles, missing coverage, strict payment terms, or discounts that do not apply after the quote is finalized.

This guide focuses on the quote comparison process: what information to prepare, how to make quotes match, which discounts to ask about, what red flags to avoid, and how to choose a policy that balances price with real protection.

Why Quote Comparison Matters More for Young Drivers

Young drivers often face higher premiums because insurers may view newer or less experienced drivers as higher risk. The Insurance Information Institute explains that teenage drivers represent a high-risk segment and that adding a teen driver can significantly increase the cost of a family policy.[1]

NHTSA says novice teen drivers are twice as likely as adult drivers to be in a fatal crash. This does not mean every young driver is unsafe, but it helps explain why insurers often price young drivers more cautiously until they build a longer, cleaner driving record.[2]

Less driving history

Newer drivers have less history for insurers to evaluate, which can make quote comparison especially important.

More pricing variation

Different insurers may rate young drivers differently, so one quote rarely tells the full story.

Coverage choices matter

A quote can look cheap because it has low limits, high deductibles, or missing optional coverage.

Prepare This Information Before Requesting Quotes

Accurate quotes require accurate information. If you change the driver list, vehicle details, garaging address, coverage limits, or deductible from one quote to another, the prices will not be easy to compare.

Quote preparation checklist

- Driver name, age, license status, and driving history.

- Vehicle year, make, model, trim, VIN, safety features, and ownership status.

- Garaging address, school address if relevant, and expected mileage.

- Whether the car is financed, leased, or fully paid off.

- Current insurance status and whether there has been a coverage lapse.

- Desired liability limits, deductibles, collision, comprehensive, and uninsured motorist coverage.

- Student status, grades, driver training, telematics interest, and possible household discounts.

A quote based on incomplete or incorrect information can change later. Use the same drivers, vehicle, address, limits, deductibles, and payment schedule when comparing companies.

Make Every Quote Use the Same Coverage

The National Association of Insurance Commissioners recommends comparing coverage, deductibles, and total premium when shopping for auto insurance. It also reminds consumers that higher deductibles can lower premiums but require more out-of-pocket payment after a claim.[3]

| Quote Detail | What to Match | Why It Matters |

|---|---|---|

| Liability limits | Use the same bodily injury and property damage limits. | A state-minimum quote can look cheaper than a quote with stronger liability protection. |

| Collision coverage | Confirm whether it is included and use the same deductible. | Collision may matter if the vehicle is financed, leased, newer, or hard to replace. |

| Comprehensive coverage | Confirm whether it is included and use the same deductible. | Comprehensive may help with theft, vandalism, fire, hail, falling objects, and animal damage. |

| Uninsured motorist coverage | Compare whether it is included, optional, rejected, or required by state rules. | Removing it may lower price but can reduce protection after an accident with an uninsured driver. |

| Payment schedule | Compare full premium, first payment, fees, and monthly installments. | A low first payment may not mean the lowest total cost. |

Choose Deductibles You Can Actually Afford

A deductible is the amount you pay out of pocket before insurance pays for a covered collision or comprehensive claim. A higher deductible can reduce the premium, but it can create a problem if the young driver cannot afford that amount after an accident.

| Deductible Choice | Possible Benefit | Risk to Consider |

|---|---|---|

| Lower deductible | Less out of pocket after a covered claim. | Premium may be higher. |

| Higher deductible | Premium may be lower. | The driver must pay more after a claim. |

| No collision or comprehensive | Premium may drop. | Your own vehicle may not be covered after many losses. |

If a $1,000 deductible would be impossible to pay after a crash, a slightly higher premium with a lower deductible may be more realistic.

Ask About Young Driver Discounts

Discounts vary by insurer and state. III explains that driver education and good student discounts may help reduce the cost impact for teen drivers, and that it is generally cheaper to put a teenage driver on a family policy than to buy a separate policy.[4]

Discounts and strategies to ask about

- Good student discount.

- Driver education or defensive driving discount.

- Safe driver or accident-free discount.

- Student away at school discount.

- Multi-vehicle or family policy pricing.

- Multi-policy discount for renters, home, or condo insurance.

- Low-mileage or usage-based insurance discount.

- Paid-in-full, autopay, paperless, or electronic document discount.

For a deeper savings guide, review cheap car insurance for young drivers and compare those strategies against the quotes you receive.

Family Policy vs. Separate Policy

For many young drivers, the biggest quote difference is whether they are added to a family policy or buy a separate policy. This depends on household rules, vehicle ownership, state requirements, insurer underwriting, and whether the young driver lives at home, away at school, or independently.

| Option | Potential Advantage | What to Confirm |

|---|---|---|

| Added to family policy | Often cheaper than a separate teen policy and may qualify for household discounts. | Which vehicle the driver is assigned to and how much the household premium increases. |

| Separate policy | Can separate billing and coverage from the family policy. | Whether the young driver has enough insurance history and can afford the full cost. |

| Student away at school | May reduce cost if the student does not regularly drive the household car. | Distance requirements, vehicle location, and how often the student drives. |

| Young adult with own vehicle | May build independent insurance history. | Whether bundling, telematics, or safer vehicle choice can lower the quote. |

If a young driver regularly uses a household vehicle, ask the insurer how that driver should be listed. Omitting regular drivers can create claim and cancellation problems.

Be Careful With Telematics Quotes

Usage-based insurance, also called telematics, can track mileage and driving behavior through a device, built-in vehicle technology, or a mobile app. NAIC explains that telematics may collect information such as miles driven, time of day, where the vehicle is driven, rapid acceleration, hard braking, hard cornering, and other driving behavior.[5]

Before enrolling in telematics, ask:

- What data is collected?

- Can the discount disappear at renewal?

- Can the premium increase if the score is poor?

- Does the program track phone use, location, time of day, or hard braking?

- Who can access the data?

- Can you leave the program later?

It can help some careful drivers, but it should be reviewed like any other policy feature. Ask whether the program can raise rates as well as lower them.

Young Driver Quote Red Flags

A quote can be cheap for the wrong reasons. Before choosing the lowest price, review what may be missing or unrealistic.

Minimum liability may satisfy the law but may not provide enough protection after a serious accident.

A high deductible can lower the premium but create a financial problem after a covered claim.

A quote may change if good student, driver training, or telematics discounts are not approved.

Liability-only coverage usually does not repair your own car after an at-fault crash.

A quote is not active coverage. Confirm when the policy starts and when proof of insurance is issued.

Before buying, verify the insurer or agent is licensed and that the policy details are clear.

Evaluate the Insurance Company, Not Only the Price

The cheapest quote is not always the best quote. NAIC recommends verifying that the agent and insurance company are licensed through your state insurance department and comparing coverage details before buying.[6]

| Company Factor | What to Look For | Warning Sign |

|---|---|---|

| Licensing | Company or agent is authorized to sell insurance in your state. | No clear license information or pressure to pay before details are confirmed. |

| Claims process | Clear claim reporting, repair steps, and communication options. | Confusing policy documents or many unresolved service complaints. |

| Policy clarity | Declarations page clearly shows limits, deductibles, drivers, vehicles, and dates. | Very low price with vague coverage details. |

| Payment terms | Fees, due dates, cancellation rules, and renewal process are clear. | Low first payment but high fees or strict cancellation terms. |

Before You Buy: Final Quote Checklist

Use this checklist before choosing a policy. The goal is to avoid comparing a strong quote against a weak one or choosing a cheap quote that does not fit your real driving needs.

Confirm before paying:

- The quote includes the correct driver, vehicle, garaging address, and mileage.

- The policy meets your state’s insurance requirements.

- The liability limits are realistic for your risk, not only the legal minimum.

- Collision and comprehensive are included if the car is financed, leased, newer, or hard to replace.

- The deductible is an amount the driver or household could afford after a claim.

- All discounts are confirmed or clearly listed as pending.

- The policy start date and proof of insurance timing are clear.

- The insurer or agent is licensed in your state.

- The full six-month or annual cost is compared, not only the first payment.

If the main issue is upfront cost, compare flexible car insurance payment options carefully and make sure the full policy cost still makes sense.

Frequently Asked Questions

How many car insurance quotes should young drivers compare?

Comparing at least three quotes can help young drivers see how much pricing varies. The quotes should use the same drivers, vehicle, address, limits, deductibles, and optional coverage.

Why do young driver quotes vary so much?

Insurers use different rating methods, discounts, underwriting rules, and risk models. Age, driving experience, vehicle type, location, coverage choices, and driving record can all affect the final price.

Is the cheapest quote always the best option?

No. The cheapest quote may have low liability limits, high deductibles, missing collision or comprehensive coverage, or payment terms that increase lapse risk.

Should a young driver stay on a family policy?

Often it can be cheaper, especially for teen drivers, but it depends on household rules, vehicle assignment, insurer pricing, and whether the young driver has their own car or lives away from home.

Can telematics help young drivers save money?

It can help some careful drivers, but young drivers should ask what data is collected, whether the rate can increase, and whether the discount continues at renewal.

What should young drivers avoid when comparing quotes?

Avoid comparing unmatched policies, hiding regular drivers, choosing unaffordable deductibles, relying on unverified discounts, or driving before the policy is active.

Final Thoughts on Comparing Young Driver Car Insurance Quotes

Young drivers should compare car insurance quotes with more than price in mind. A quote should be judged by coverage limits, deductibles, vehicle protection, discounts, company reliability, payment terms, and how well the policy fits the driver’s real situation.

The best quote is not always the lowest quote. It is the one that gives a young driver legal coverage, realistic protection, clear terms, and a payment structure that can be maintained without a lapse.

Compare Auto Insurance Options Carefully

Before choosing a policy, compare the full cost, coverage limits, deductibles, discounts, payment terms, and proof-of-insurance timing.

Compare Auto Insurance OptionsReferences

- Insurance Information Institute, Students. Source ↩

- National Highway Traffic Safety Administration, Teen Driving. Source ↩

- National Association of Insurance Commissioners, Comparing Online Auto Insurance Quotes. Source ↩

- Insurance Information Institute, Students. Source ↩

- National Association of Insurance Commissioners, Understanding Usage-Based Insurance. Source ↩

- National Association of Insurance Commissioners, A Shopping Tool for Auto Insurance. Source ↩