Comprehensive car insurance helps pay for certain damage to your own vehicle that is not caused by a collision. It is often discussed with collision coverage, but the two cover different risks.

This guide explains what comprehensive coverage usually covers, what it does not cover, how deductibles work, when lenders may require it, and when it may or may not be worth adding to an auto insurance policy.

Quick Summary

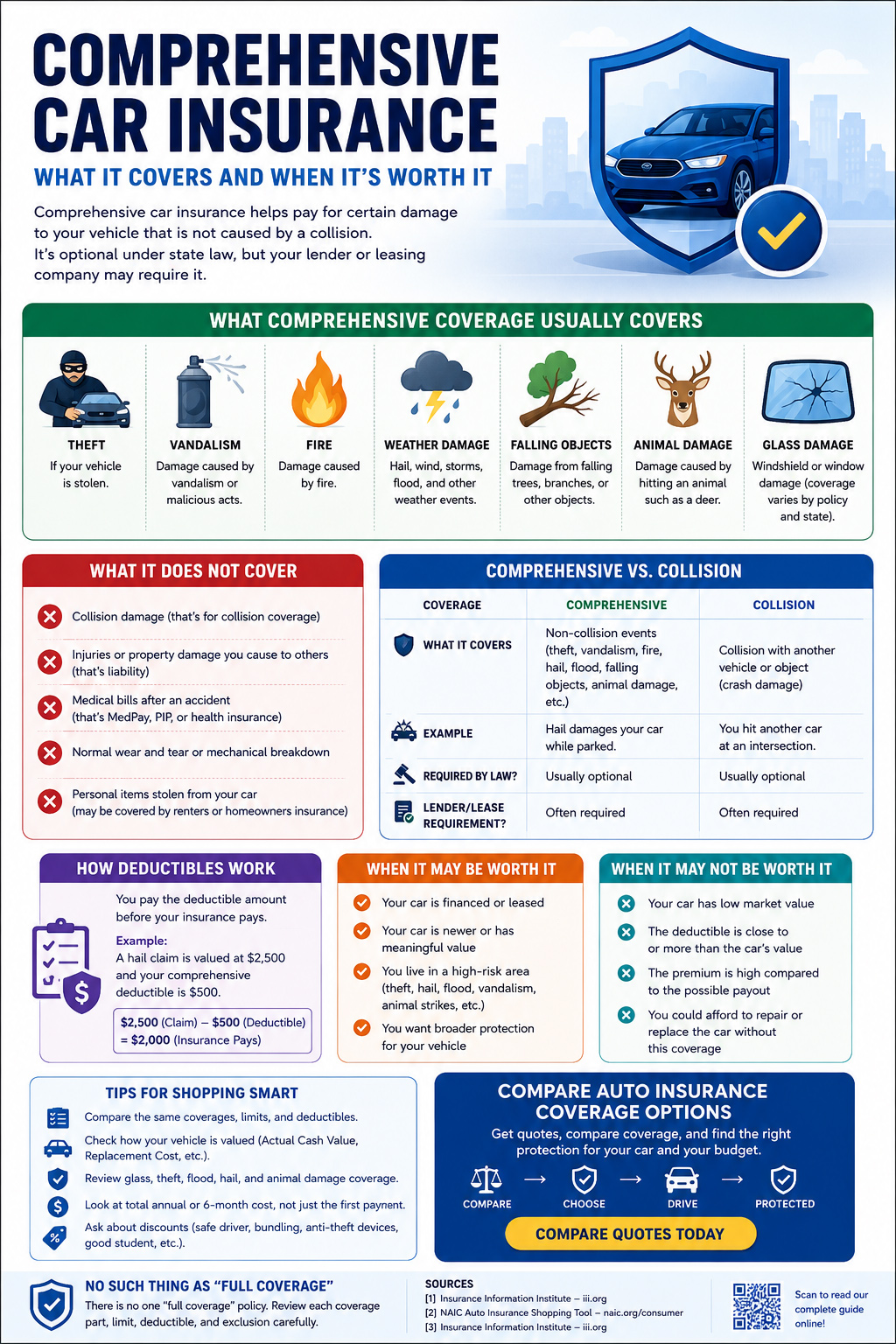

- Comprehensive coverage generally helps pay for damage to your car from non-collision events, such as theft, vandalism, fire, hail, wind, falling objects, flood, or contact with an animal.

- It is different from collision coverage, which generally applies when your vehicle hits another car or object.

- Comprehensive coverage usually has a deductible, which is the amount you pay before insurance applies to a covered claim.

- State law usually focuses on liability coverage, but lenders or leasing companies may require comprehensive and collision while the vehicle is financed or leased.

- Comprehensive may be more useful for newer, financed, leased, or higher-value vehicles than for older cars with low market value.

What Is Comprehensive Car Insurance?

Comprehensive car insurance, sometimes called “other than collision” coverage, helps pay for certain damage to your own vehicle that is not caused by a crash with another vehicle or object. The NAIC describes comprehensive as coverage for damage to your car that is not from a collision.[1]

Comprehensive is not the same as liability insurance. Liability coverage helps pay for injuries or property damage you cause to others, up to policy limits. Comprehensive coverage is for your own vehicle, subject to the policy’s terms, exclusions, and deductible.

Your own vehicle

Comprehensive generally protects your car, not another driver’s car or medical bills.

Non-collision events

The coverage is usually tied to events like theft, vandalism, weather, fire, falling objects, flood, or animal damage.

Usually optional

It may be optional under state law, but your lender or leasing company may require it if the car is financed or leased.

What Comprehensive Car Insurance Usually Covers

Policy wording varies by insurer, but comprehensive coverage generally applies to covered non-collision damage to your car. The NAIC lists examples such as fire, theft, wind, hail, hitting a deer, vandalism, and theft when explaining comprehensive protection.[2]

| Covered Event | How It May Apply | What to Check |

|---|---|---|

| Theft | May help pay if your car is stolen and the claim meets policy terms. | Deductible, claim documentation, waiting period, and valuation method. |

| Vandalism | May help repair damage caused by vandalism or malicious acts. | Police report requirements and excluded situations. |

| Fire | May help with covered fire damage to the vehicle. | Cause of fire, exclusions, and claim investigation rules. |

| Weather damage | May help with hail, wind, flood, or certain storm-related damage. | Deductible, flood wording, storage location, and state-specific rules. |

| Falling objects | May help if a tree branch or other falling object damages the vehicle. | Whether the event is covered and what proof is needed. |

| Animal damage | May help after certain animal-related damage, such as hitting a deer. | Whether the policy treats the loss as comprehensive rather than collision. |

| Glass damage | May help with windshield or window damage, depending on the policy. | Glass deductible, repair vs. replacement rules, and state-specific glass rules. |

Comprehensive coverage does not mean every non-collision loss is automatically covered. Exclusions, deductibles, limits, proof requirements, and claim conditions still matter.

What Comprehensive Insurance Does Not Cover

Comprehensive coverage has limits. It does not replace liability, collision, medical payments, personal injury protection, or uninsured motorist coverage. It also does not turn a policy into coverage for every possible loss.

| Not Usually Covered by Comprehensive | Why It Matters | Coverage to Review Instead |

|---|---|---|

| Damage you cause to another person’s car | Comprehensive protects your vehicle, not another driver’s property. | Property damage liability. |

| Injuries to other people | Comprehensive does not pay bodily injury liability claims. | Bodily injury liability. |

| Collision with another vehicle or object | Crash damage to your own vehicle generally belongs under collision coverage. | Collision coverage. |

| Your medical bills after a crash | Comprehensive is vehicle damage coverage, not medical coverage. | Medical payments, PIP, or health coverage depending on state and policy. |

| Normal wear and tear | Insurance usually does not pay for ordinary aging, maintenance, or mechanical breakdown. | Maintenance plan, warranty, or mechanical breakdown coverage if available. |

| Personal items stolen from the car | Items inside the vehicle may not be covered by auto comprehensive coverage. | Renters or homeowners insurance may apply, subject to policy terms. |

The NAIC reminds consumers that there is no single auto policy officially called “full coverage.” A policy is made of separate coverage parts, and each one has its own limits, exclusions, and deductibles.[3]

Comprehensive vs. Collision Coverage

Comprehensive and collision are often purchased together, especially for financed or leased vehicles, but they cover different types of damage. The NAIC explains that collision coverage pays to repair your car after covered collision damage, while comprehensive pays for damage that is not from a collision.[4]

| Coverage | General Purpose | Example |

|---|---|---|

| Comprehensive | Helps pay for covered non-collision damage to your own car. | Your car is damaged by hail, theft, vandalism, fire, flood, a falling branch, or a deer. |

| Collision | Helps pay for covered crash damage to your own car. | Your car hits another vehicle, a pole, a fence, or another object. |

| Liability | Helps pay for injuries or property damage you cause to others, up to policy limits. | You are at fault for an accident that damages another driver’s vehicle. |

How the Comprehensive Deductible Works

Comprehensive coverage usually includes a deductible. The deductible is the part of a covered claim you pay before the insurance payout applies. For example, if a covered theft or hail claim is valued at $3,000 and your deductible is $500, the insurer’s payment may be based on the remaining covered amount, subject to policy terms.

Higher deductible

May lower the premium, but you pay more out of pocket after a covered claim.

Lower deductible

May cost more each month, but it can reduce your out-of-pocket claim cost.

Glass claims

Some policies or states may treat glass claims differently, so review windshield rules carefully.

Choose a deductible you could realistically pay after a claim. A deductible that is too high can make the coverage less useful when you need it.

When Comprehensive Coverage May Be Worth It

Comprehensive coverage may be worth comparing if your vehicle would be expensive to replace, if it is financed or leased, or if the car is exposed to theft, hail, flooding, vandalism, animal collisions, or other non-collision risks.

Lenders and leasing companies commonly require comprehensive and collision until the loan or lease obligation is satisfied.

If replacing the car would be financially difficult, comprehensive may offer useful protection.

Theft, hail, flood exposure, falling trees, or animal strikes may make comprehensive more valuable.

Comprehensive can help protect against non-crash events that liability-only coverage does not cover.

When Comprehensive Coverage May Not Be Worth It

Comprehensive may be less useful when a car has a very low market value, the deductible is close to the car’s value, or the premium is high compared with the possible payout. Drivers with older paid-off vehicles should compare the cost of the coverage with the vehicle’s realistic value.

Questions to ask before dropping comprehensive

- Is the vehicle financed or leased?

- What is the car’s current market value?

- How much is the comprehensive premium for the policy term?

- What deductible would apply after a claim?

- Could I afford to repair or replace the car without this coverage?

- Is the car exposed to theft, hail, flood, vandalism, falling objects, or animal-related risks?

Comprehensive Insurance and “Full Coverage”

Many drivers use “full coverage” to mean a policy that includes liability, collision, and comprehensive coverage. However, “full coverage” is not a single standardized policy. The NAIC specifically warns that there is no such thing as “full coverage.”[5]

A policy with comprehensive and collision may still exclude certain losses, apply deductibles, have limits, or leave gaps. That is why it is better to compare the actual coverage parts instead of relying on the phrase “full coverage.”

| Phrase | What It Often Means | What to Verify |

|---|---|---|

| Liability-only | Usually means coverage for injuries or property damage you cause to others. | State minimums, higher limits, uninsured motorist, and medical coverage. |

| Comprehensive and collision | Usually means your own car has physical damage protection for covered events. | Deductibles, exclusions, vehicle value, lender requirements, and covered causes of loss. |

| Full coverage | Often used informally for liability plus comprehensive and collision. | There is no universal “full coverage” policy. Review every coverage part separately. |

How to Compare Comprehensive Car Insurance Quotes

When comparing quotes, do not look only at the monthly payment. A cheaper quote may have a higher deductible, lower vehicle valuation, fewer endorsements, weaker glass coverage, stricter exclusions, or missing collision coverage.

Comprehensive quote checklist

- Compare the same liability limits, collision coverage, comprehensive coverage, and deductibles.

- Check whether the car is valued using actual cash value, stated amount, or another method.

- Ask how glass claims, windshield repair, and replacement are handled.

- Review theft, flood, hail, fire, vandalism, animal, and falling-object coverage.

- Confirm whether the lender or leasing company requires comprehensive and collision.

- Compare the full six-month or annual premium, not only the first payment.

- Check whether discounts apply for anti-theft devices, bundling, safe driving, or telematics.

For a broader overview of liability, collision, deductibles, discounts, and other coverage types, see our car insurance guide.

Common Mistakes to Avoid

Comprehensive coverage is useful only when the driver understands what it does and does not do. These mistakes can lead to confusion, weak protection, or unexpected out-of-pocket costs.

| Mistake | Why It Can Hurt | Better Approach |

|---|---|---|

| Thinking comprehensive means full protection | Comprehensive does not cover every type of loss. | Review liability, collision, medical, uninsured motorist, and exclusions separately. |

| Dropping coverage on a financed car | This may violate a loan or lease agreement. | Check lender or lease requirements before changing coverage. |

| Choosing a deductible that is too high | A claim can become unaffordable if the deductible is unrealistic. | Choose a deductible based on actual emergency savings. |

| Not checking glass rules | Windshield rules can vary by policy and state. | Ask how repair, replacement, and deductible rules apply. |

| Ignoring the car’s value | Coverage may not be cost-effective on a very low-value vehicle. | Compare premium, deductible, and realistic payout value. |

Final Thoughts on Comprehensive Car Insurance

Comprehensive car insurance can be valuable if your vehicle is financed, leased, newer, higher-value, or exposed to theft, weather, vandalism, fire, flood, falling objects, or animal-related damage. It is not a replacement for liability or collision coverage, and it does not guarantee every type of loss will be paid.

The best approach is to compare comprehensive coverage as one part of the full policy. Review deductibles, exclusions, vehicle value, lender requirements, claim rules, and total cost before deciding whether to add, keep, change, or remove it.

Simple rule

Comprehensive coverage may be worth it when the cost of protecting the car is reasonable compared with the risk of losing or repairing it after a covered non-collision event.

Compare Auto Insurance Coverage Options

Before choosing a policy, compare liability limits, comprehensive coverage, collision coverage, deductibles, discounts, payment terms, and the total policy cost.

Frequently Asked Questions

Is comprehensive car insurance required by law?

State law usually focuses on liability insurance requirements. Comprehensive coverage is usually optional under state law, but a lender or leasing company may require it while the vehicle is financed or leased.

Does comprehensive insurance cover accidents?

Comprehensive generally covers certain non-collision events. Damage from a crash with another car or object is usually handled under collision coverage, not comprehensive coverage.

Does comprehensive cover theft?

Comprehensive may help if your vehicle is stolen, subject to policy terms, exclusions, deductible, claim documentation, and valuation rules.

Does comprehensive cover hail damage?

Comprehensive may help with covered hail damage to your vehicle, subject to the deductible and policy terms.

Is comprehensive the same as full coverage?

No. Comprehensive is one coverage part. “Full coverage” is an informal phrase and does not describe one standardized policy. A driver should review each coverage, limit, deductible, and exclusion separately.

Should I keep comprehensive on an older car?

It depends on the car’s value, the premium, the deductible, your financial situation, and whether the vehicle is financed or leased. If the car has very low value, compare the possible payout with the cost of keeping the coverage.

References

- [1] National Association of Insurance Commissioners, “A Shopping Tool for Auto Insurance.” Source ↩

- [2] National Association of Insurance Commissioners, “Auto Insurance.” Source ↩

- [3] National Association of Insurance Commissioners, “A Shopping Tool for Auto Insurance.” Source ↩

- [4] National Association of Insurance Commissioners, “Automobile Insurance Shopping Tool.” Source ↩

- [5] Insurance Information Institute, “Auto insurance basics—understanding your coverage.” Source ↩