By Young Americans Insurance Editorial Team

Published on · Updated on

This commercial truck insurance guide was reviewed for current FMCSA filing references, coverage clarity, quote-comparison usefulness, and consumer/business disclosure quality.

Commercial truck insurance protects trucking businesses, owner-operators, and fleets from major financial risks tied to accidents, vehicle damage, cargo loss, liability claims, regulatory filings, and contract requirements.

The right policy depends on your operating authority, vehicle weight, cargo type, state rules, routes, contracts, driver history, and whether you operate interstate or intrastate. This guide explains the coverage areas, FMCSA filing issues, cost factors, and quote red flags to review before buying a policy.

Understanding Commercial Truck Insurance

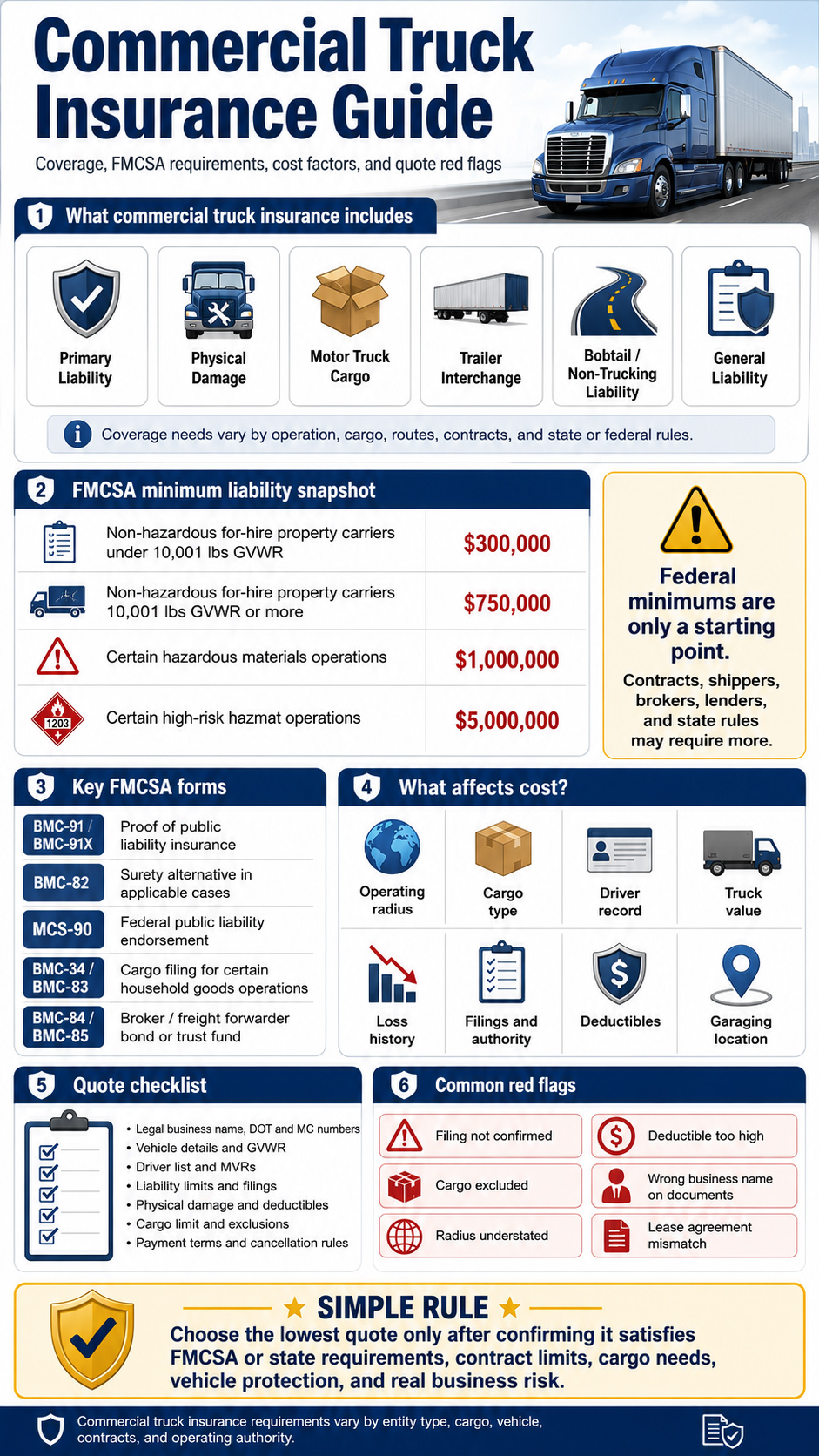

Commercial truck insurance is not one single coverage. It is usually a package of policies, endorsements, filings, and limits built around the truck, driver, business operation, cargo, contract requirements, and federal or state rules. A local delivery business, an owner-operator under lease, a household goods mover, and an interstate freight carrier may all need different insurance structures.

FMCSA says insurance requirements vary depending on entity type, operating authority, cargo type, and vehicle type. FMCSA also states that operating authority registration will not be granted until the registrant has the required minimum financial responsibility on file with FMCSA.[1]

That means a trucking business should not compare policies by price alone. The quote should be reviewed for liability limits, filings, physical damage, cargo, trailer interchange, non-trucking liability, bobtail exposure, deductibles, exclusions, driver rules, certificate turnaround time, and claim handling.

Authority matters

Interstate for-hire carriers may need FMCSA filings, while intrastate operations may follow state-specific rules.

Cargo matters

Non-hazardous freight, household goods, refrigerated loads, high-value cargo, and hazardous materials can create different insurance needs.

Contracts matter

Shippers, brokers, leases, lenders, and motor carriers may require limits above legal minimums.

Federal Insurance Requirements for Interstate Trucking

Federal minimums are a starting point, not a complete insurance program. FMCSA’s insurance filing chart lists different BIPD liability requirements for different carrier types. Non-hazardous for-hire property carriers under 10,001 pounds GVWR are listed at $300,000, while non-hazardous for-hire property carriers at or above 10,001 pounds GVWR are listed at $750,000. Certain hazardous materials carriers are listed at $1,000,000 or $5,000,000 depending on the operation and commodity.[2]

| Operation Type | FMCSA Filing / Limit Snapshot | Important Note |

|---|---|---|

| For-hire property carrier, non-hazardous, under 10,001 lbs GVWR | $300,000 BIPD requirement listed by FMCSA. | State rules, contracts, and insurers may require more. |

| For-hire property carrier, non-hazardous, 10,001 lbs GVWR or more | $750,000 BIPD requirement listed by FMCSA. | Many shippers and brokers require $1 million or more by contract. |

| Certain hazardous materials carriers | $1,000,000 BIPD requirement listed by FMCSA. | Hazmat operations need specialized underwriting and filings. |

| Explosives, poison gas, radioactive materials, or certain high-risk hazmat operations | $5,000,000 BIPD requirement listed by FMCSA. | Specialized filings, underwriting, and safety compliance review are usually required. |

| Household goods carrier, 10,001 lbs GVWR or more | $750,000 BIPD plus cargo filing requirements listed by FMCSA. | Household goods cargo filing rules are separate from normal freight cargo coverage. |

| Passenger carrier, 15 or fewer passengers for compensation | $1,500,000 listed by FMCSA. | Passenger operations are different from cargo trucking. |

| Passenger carrier, 16 or more passengers | $5,000,000 listed by FMCSA. | Higher exposure generally means higher liability requirements. |

Your broker, shipper, lender, lease agreement, cargo contract, state regulator, or safety department may require higher limits or additional coverage even when the FMCSA minimum has been satisfied.

FMCSA Filings and Forms to Know

FMCSA’s insurance filing chart lists BMC-91, BMC-91X, or BMC-82 as applicable forms for several motor carrier property and passenger operations. It also lists the MCS-90 or MCS-82 endorsement for all for-hire and interstate motor carriers.[3]

| Form or Endorsement | General Purpose | What to Confirm |

|---|---|---|

| BMC-91 or BMC-91X | Proof of public liability insurance filed by the insurer or filer. | Confirm that the filing matches the legal business name and operating authority. |

| BMC-82 | Surety bond alternative for certain public liability requirements. | Ask whether this form applies to your operation and insurer structure. |

| MCS-90 | Endorsement tied to federal motor carrier public liability responsibility. | Review with a trucking insurance professional because it is not the same as ordinary coverage for every loss. |

| BMC-34 or BMC-83 | Cargo filing forms for certain household goods operations. | Do not assume general freight cargo insurance has the same federal filing requirement. |

| BMC-84 or BMC-85 | Broker or freight forwarder surety bond or trust fund agreement. | This is separate from truck liability, physical damage, and cargo insurance. |

FMCSA cautions that business name and address mismatches in filings can delay authority. Use the exact legal business name, DBA, address, DOT number, and MC number when requesting filings.

Types of Commercial Truck Insurance Coverage

A commercial truck insurance program can include several separate coverages. Some protect other people, some protect your truck, and some protect cargo or the business operation. Mixing up these coverages can leave serious gaps.

| Coverage Type | What It Generally Does | Who Usually Needs It |

|---|---|---|

| Primary auto liability | Helps pay for bodily injury or property damage to others when the truck causes a covered accident. | Most commercial trucking operations; often required by law and contracts. |

| Physical damage | Helps repair or replace your own tractor, truck, or trailer after covered collision or non-collision damage. | Truck owners, financed trucks, leased trucks, and fleets with valuable equipment. |

| Motor truck cargo | Helps cover cargo loss or damage while goods are in your care, custody, and control. | For-hire carriers, owner-operators, and fleets hauling goods for others. |

| General liability | May cover certain business liability exposures away from driving, such as premises or completed operations. | Trucking businesses with offices, yards, contracts, or non-auto business exposure. |

| Trailer interchange | Helps cover damage to a non-owned trailer used under a trailer interchange agreement. | Carriers pulling trailers owned by others under written agreements. |

| Non-trucking liability | May apply when an owner-operator uses the truck for non-business personal use. | Leased owner-operators when the motor carrier’s primary liability does not apply. |

| Bobtail coverage | May apply when operating the tractor without a trailer, depending on policy wording. | Owner-operators who drive without a trailer between dispatches or after delivery. |

| Workers’ compensation or occupational accident | Can address driver injury exposure, depending on employment status and state law. | Fleets, employers, and some owner-operator programs. |

Primary Liability Coverage

Primary liability is usually the foundation of a trucking insurance program. It helps protect the business if the truck causes bodily injury or property damage to others. For interstate for-hire carriers, proof of the required financial responsibility generally must be filed with FMCSA by the insurer, surety, or financial responsibility provider before authority is granted.

Primary liability checklist

- Confirm whether you operate interstate, intrastate, or both.

- Check the required federal and state limits.

- Confirm whether BMC-91, BMC-91X, BMC-82, MCS-90, or MCS-82 applies.

- Review contract limits required by brokers, shippers, carriers, and leases.

- Check whether hired and non-owned auto exposure needs coverage.

- Ask how claims are handled when several parties are involved.

Physical Damage Coverage for Trucks

Physical damage coverage protects your own equipment. It is often split into collision and comprehensive coverage. Collision generally applies when the truck hits another vehicle or object. Comprehensive generally applies to non-collision losses such as theft, fire, vandalism, hail, flood, falling objects, or animal damage. NAIC explains that collision coverage is optional under law but may be required by a lender or lessor, and that collision and comprehensive coverage usually involve deductibles.[4]

If your truck is financed, leased, or expensive to replace, physical damage can be one of the most important parts of the policy. The business should also review valuation method, deductible, excluded uses, repair network, downtime exposure, and whether trailers or attached equipment are included.

| Physical Damage Component | What It Helps With | What to Check |

|---|---|---|

| Collision | Damage to your truck from a covered crash with another vehicle or object. | Deductible, valuation method, repair network, and downtime impact. |

| Comprehensive | Theft, fire, vandalism, hail, flood, falling objects, and some animal damage. | Exclusions, deductible, glass rules, weather exposure, and storage location. |

| Specified perils | Only certain listed causes of loss, depending on policy wording. | Cheaper does not always mean better; review what is excluded. |

| Downtime or rental reimbursement | May help with substitute vehicle or loss-of-use costs, depending on policy. | Waiting period, daily limit, and maximum benefit. |

Motor Truck Cargo Insurance

Cargo insurance helps protect goods being transported. It is not the same as liability insurance or physical damage coverage. A truck can be properly insured for road liability and still have a gap if the load is damaged, stolen, rejected, spoiled, or excluded by the cargo policy.

FMCSA’s chart lists a cargo filing requirement for certain household goods carriers and freight forwarders, using BMC-34 or BMC-83. For many general freight carriers, cargo insurance may be driven more by contracts, brokers, shippers, lenders, or practical business risk than by a separate federal cargo filing requirement.[5]

Cargo questions to ask before hauling

- What cargo types are covered and excluded?

- Does the policy cover theft, reefer breakdown, water damage, loading, and unloading?

- Is unattended vehicle theft excluded or limited?

- Are electronics, alcohol, pharmaceuticals, household goods, or hazmat excluded?

- Does the contract require a specific cargo limit?

- Is the deductible per load, per occurrence, or per vehicle?

- Are bills of lading, temperature logs, seal records, or inspection reports required for claims?

Bobtail vs. Non-Trucking Liability

Bobtail and non-trucking liability are often confused. The exact difference depends on policy wording and the lease agreement, so an owner-operator should never assume one automatically replaces the other.

| Coverage | Common Meaning | Example Situation |

|---|---|---|

| Bobtail coverage | May apply when the tractor is being driven without a trailer, depending on policy wording. | The driver drops a trailer and drives the tractor alone. |

| Non-trucking liability | May apply when the truck is being used for personal, non-business use. | The driver uses the tractor for a personal errand while off dispatch. |

| Primary liability from motor carrier | May apply when the leased owner-operator is operating under dispatch for the carrier. | The driver is hauling a load under the carrier’s authority. |

Owner-operators should compare the insurance policy with the lease agreement. A gap can appear when the carrier’s primary liability stops but the driver’s personal, bobtail, or non-trucking exposure continues.

Broker and Freight Forwarder Financial Responsibility

Commercial truck insurance should not be confused with broker or freight forwarder financial responsibility. FMCSA states that effective January 16, 2026, brokers, freight forwarders, and financial responsibility providers must comply with new rules regarding broker and freight forwarder financial responsibility. FMCSA’s insurance filing chart also lists a $75,000 surety bond or trust fund agreement for brokers and certain freight forwarders using BMC-84 or BMC-85.[6]

Broker bond is separate

A BMC-84 or BMC-85 broker bond or trust fund agreement is not the same as truck liability, physical damage, or cargo insurance. A company that operates trucks and brokers freight may need more than one compliance strategy.

What Affects Commercial Truck Insurance Cost?

Sample premium ranges can become misleading quickly because trucking premiums vary widely by operation. Insurers may look closely at safety history, vehicle type, operating radius, cargo, filings, driver experience, claims history, garaging location, and contract requirements.

| Cost Factor | Why It Matters | How to Manage It |

|---|---|---|

| Operating radius | Longer routes and interstate operations can increase exposure. | Quote accurately and do not understate your radius. |

| Cargo type | High-value, refrigerated, hazardous, or theft-prone cargo can cost more. | Match cargo coverage to contracts and actual loads. |

| Driver record | Tickets, crashes, violations, and experience affect underwriting. | Screen drivers and document safety training. |

| Truck value | Higher-value tractors and trailers cost more to repair or replace. | Review stated amount, actual cash value, and deductibles. |

| Loss history | Frequent or severe claims can increase premiums or reduce options. | Build a safety program and track corrective action. |

| Filings and authority | FMCSA and state filings can limit which insurers can write the policy. | Work with an agent who understands trucking filings. |

| Deductibles | Higher deductibles may reduce premiums but increase claim costs. | Choose deductibles the business can actually pay. |

How to Compare Commercial Truck Insurance Quotes

A cheaper quote may be missing coverage, filings, cargo endorsements, hired auto coverage, trailer interchange, or the correct operating radius. Compare each quote line by line before choosing the lowest price.

Quote comparison checklist

- Exact legal business name, DOT number, MC number, and operating authority.

- Vehicle year, make, model, VIN, GVWR, value, garaging address, and radius.

- Driver list, CDL status, MVRs, experience, and violation history.

- Primary liability limits and required filings.

- Physical damage coverage, deductible, and valuation method.

- Cargo limit, exclusions, deductible, and special load requirements.

- Trailer interchange, non-owned trailer, bobtail, or non-trucking liability needs.

- General liability, workers’ compensation, occupational accident, or umbrella needs.

- Monthly fees, down payment, cancellation rules, and certificate turnaround time.

Common Mistakes Trucking Businesses Should Avoid

Commercial trucking policies are detailed. A mistake can cause a denied claim, delayed authority, contract issue, or expensive coverage gap.

| Mistake | Why It Can Hurt | Better Approach |

|---|---|---|

| Buying only the legal minimum | Contracts or real accident exposure may require higher limits. | Compare legal, contractual, and practical business needs. |

| Assuming cargo is covered | Liability and physical damage do not automatically cover the load. | Buy motor truck cargo coverage that matches your freight. |

| Misclassifying operations | Wrong radius, cargo, or authority can create underwriting and claim problems. | Quote the actual operation honestly. |

| Ignoring filings | Authority can be delayed or affected if filings are not handled correctly. | Confirm required FMCSA and state filings before operating. |

| Choosing deductibles too high | A claim can create a cash-flow problem if the deductible is unaffordable. | Set deductibles based on reserves, not just premium savings. |

| Not checking exclusions | Reefer breakdown, unattended theft, certain cargo, or personal use may be excluded. | Read exclusions and add endorsements where needed. |

Documents to Prepare Before Getting a Quote

Commercial truck insurance quotes are easier and more accurate when the business prepares the right documents. Missing information can delay binding, certificates, and filings.

Prepare these items

- Business legal name, DBA, address, DOT number, and MC number.

- Vehicle schedule with VINs, values, GVWR, and garaging locations.

- Driver list with CDL details, date of birth, and driving history.

- Loss runs from current or prior insurers.

- Current declarations pages and certificates.

- Type of freight hauled and any excluded cargo concerns.

- Operating radius, states traveled, and annual mileage.

- Contracts from shippers, brokers, lenders, leases, or motor carriers.

- Requested filings, certificates, and additional insured requirements.

Commercial Truck Insurance Red Flags

A low quote can be useful, but it can also hide a serious coverage problem. Before binding commercial truck insurance, review the main red flags carefully.

The policy may not satisfy FMCSA or state filing needs if the required forms are not filed correctly.

Some cargo types may be excluded, sublimited, or subject to strict claim conditions.

Quoting a smaller operating radius than the business actually uses can create underwriting and claim problems.

A high deductible can lower premium but create a cash-flow problem after a claim.

Business name, address, DOT number, and MC number must match filings and documents.

Owner-operators should compare the insurance policy with the lease agreement before assuming coverage applies.

How to Lower Commercial Truck Insurance Costs Safely

Lowering premiums should not create coverage gaps. The goal is to improve the risk profile, avoid claims, and compare accurate quotes without removing protection the business needs.

Cost-control strategies

- Maintain clean MVRs and screen drivers carefully.

- Use written safety policies, driver training, and inspection routines.

- Track maintenance and repair records.

- Use dashcams, telematics, GPS, and anti-theft tools where appropriate.

- Choose deductibles the business can afford after a claim.

- Avoid hauling cargo that is excluded or outside your underwriting class.

- Compare quotes before renewal, but match coverage and filings carefully.

- Pay on time to avoid cancellation, reinstatement issues, or authority problems.

Final Thoughts on Commercial Truck Insurance

Commercial truck insurance requires more than a basic liability quote. A trucking business should review federal and state filings, primary liability, physical damage, cargo insurance, bobtail or non-trucking liability, trailer coverage, deductibles, exclusions, certificate requirements, and contract limits before choosing a policy.

The safest approach is to work with a licensed insurance professional who understands trucking operations and can verify the right filings, limits, and endorsements before the truck is dispatched.

Simple rule

Choose the lowest quote only after confirming it satisfies FMCSA or state requirements, contract limits, cargo needs, vehicle protection, and real business risk.

Frequently Asked Questions

What is the minimum liability coverage required for commercial trucks?

It depends on the operation. FMCSA’s chart lists $300,000 for certain non-hazardous for-hire property carriers under 10,001 pounds GVWR, $750,000 for non-hazardous for-hire property carriers at or above 10,001 pounds GVWR, and higher limits for certain hazardous materials operations.

What is the difference between physical damage and cargo insurance?

Physical damage helps protect your own truck or trailer. Cargo insurance helps protect goods being transported. A truck can have physical damage coverage and still need separate cargo coverage.

Do I need commercial truck insurance if I lease my truck?

It depends on the lease agreement and how the truck is used. Review who provides primary liability, whether you need non-trucking liability or bobtail coverage, and whether you are responsible for physical damage.

What is an MCS-90?

The MCS-90 is an endorsement tied to federal motor carrier public liability responsibility. It should be reviewed with a trucking insurance professional because it is not the same as ordinary first-party coverage for every loss.

Is cargo insurance required for every commercial truck?

Not always as a separate federal cargo filing. FMCSA lists cargo filing requirements for certain household goods operations, while many general freight cargo limits are driven by contracts, brokers, shippers, and practical business risk.

How can I lower commercial truck insurance costs?

Keep clean driver records, document maintenance, improve safety programs, use telematics or cameras where appropriate, compare quotes accurately, avoid excluded cargo, and choose deductibles the business can afford.

Compare Commercial Truck Insurance Carefully

Before binding coverage, compare filings, liability limits, physical damage, cargo coverage, deductibles, exclusions, certificates, and payment terms. A cheaper policy can cost more if it leaves a trucking business exposed.

Ask About Insurance ResourcesReferences

- [1] FMCSA, Insurance Filing Requirements. Source ↩

- [2] FMCSA, Insurance Filing Requirements Chart. Source ↩

- [3] FMCSA, Insurance Filing Requirements Chart and Endorsement Forms. Source ↩

- [4] NAIC, Auto Insurance. Source ↩

- [5] FMCSA, Household Goods and Cargo Filing Requirements. Source ↩

- [6] FMCSA, Broker and Freight Forwarder Financial Responsibility Rule Overview. Source ↩