By Young Americans Insurance Editorial Team

Published on · Updated on

This guide was reviewed for payment-plan clarity, coverage accuracy, consumer finance warnings, auto insurance disclosure quality, and quote-comparison usefulness.

Buy Now Pay Later Car Insurance: What It Really Means

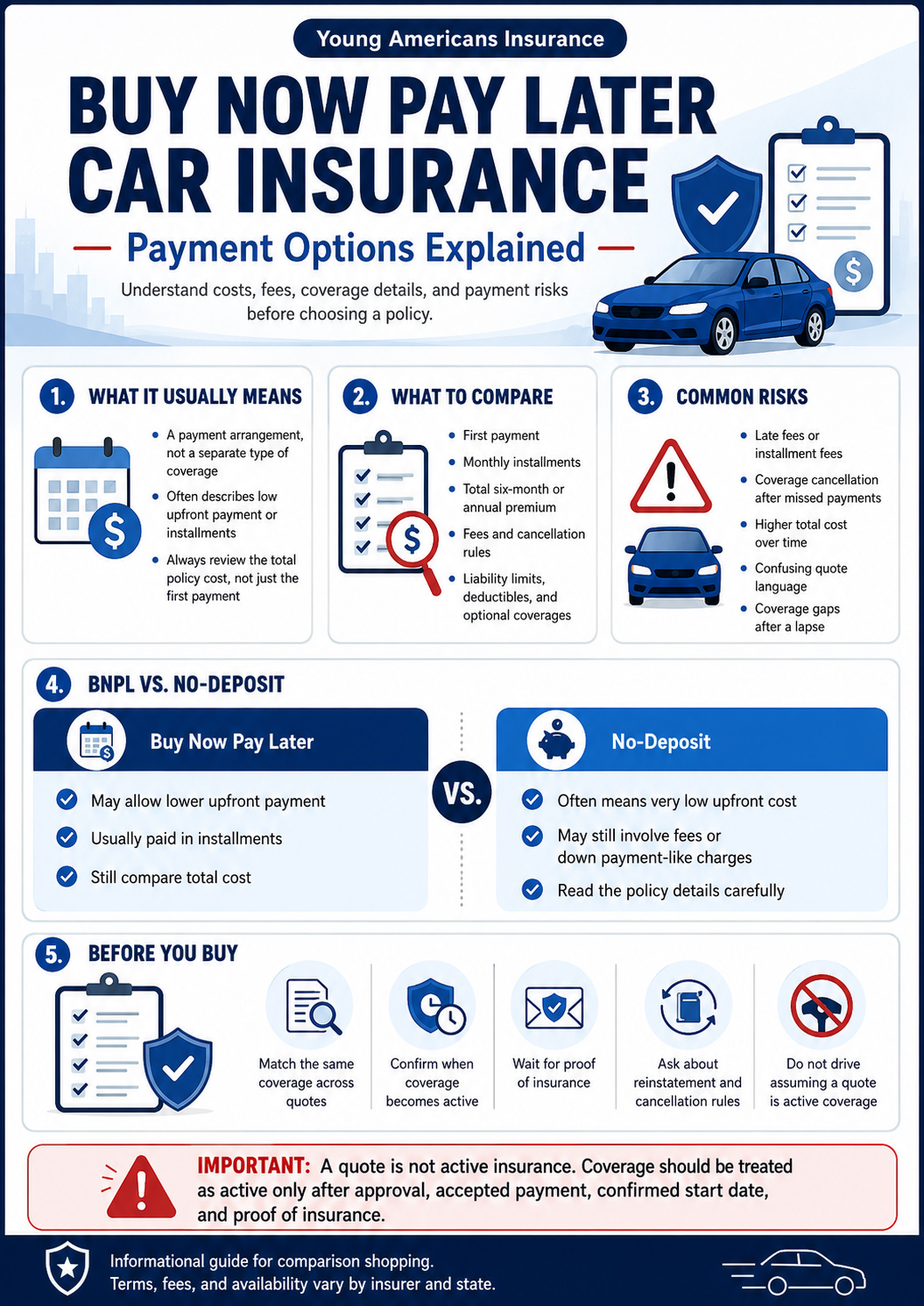

Buy now pay later car insurance is not a separate type of auto insurance coverage. It usually describes a payment arrangement, such as monthly installments, a low first payment, or premium financing. Before choosing a policy, compare the total premium, fees, cancellation rules, coverage limits, deductibles, proof of insurance rules, and payment schedule.

Quick Summary

- “Buy now pay later car insurance” usually means paying your auto insurance premium in installments, not buying a special type of coverage.

- A low first payment can help with cash flow, but it may come with installment fees, finance charges, late fees, or a higher total policy cost.

- A quote is not proof of insurance. Coverage should be considered active only after the policy is bound, the required payment is accepted, and proof of insurance is issued.

- Do not choose a policy based only on the first payment. Compare liability limits, deductibles, optional coverages, billing fees, cancellation rules, and the total six-month or annual cost.

What Is Buy Now Pay Later Car Insurance?

Buy now pay later car insurance usually refers to an auto insurance policy that lets a driver start coverage with an initial payment and then pay the remaining premium over time. In practice, this may appear as monthly installments, a low down payment, premium financing, or a billing plan offered by an insurer, agency, or finance company.

The Consumer Financial Protection Bureau describes buy now pay later as a form of short-term financing where payments are split over time. The CFPB also warns that many BNPL loans charge late fees when payments are missed, so drivers should make sure they can afford every scheduled payment before agreeing to a payment plan. [1]

Payment method

BNPL-style auto insurance is mainly about how the premium is paid, not a different type of auto coverage.

Coverage still matters

The policy should still meet state requirements and provide enough protection for your vehicle, household, and financial situation.

Missed payments can hurt

Late or missed payments may trigger fees, cancellation, loss of proof of insurance, or a coverage lapse.

Buy Now Pay Later vs. No-Deposit Car Insurance

These phrases are often used together online, but they do not always mean the same thing. “Buy now pay later” usually points to a payment schedule. “No deposit” often means a lower first payment, but most insurers still require some amount before coverage is active.

| Term | What It Usually Means | What to Confirm |

|---|---|---|

| Buy now pay later car insurance | The driver may start a policy with an initial payment and then pay the remaining premium in scheduled installments. | Payment dates, fees, cancellation rules, proof of insurance timing, and total policy cost. |

| No-deposit car insurance | Often a marketing phrase for low upfront payment options, not free coverage. | Whether any payment, binding amount, or fee is required before the policy starts. |

| Monthly car insurance payments | The premium is divided into monthly installments instead of being paid in full. | Installment fees, autopay requirements, late payment rules, and renewal billing. |

| Premium financing | A finance company may pay the insurer, and the driver repays the finance company over time. | Interest, finance charges, missed-payment consequences, and cancellation authority. |

Drivers specifically comparing low upfront payment language can also review cheap car insurance with no deposit, but this BNPL guide focuses on payment schedules, fees, proof of insurance timing, and cancellation risks.

How BNPL Car Insurance Payments Usually Work

Most drivers do not pay an entire policy term in one payment. Instead, they may make an initial payment and then pay the remaining premium over time. The important part is to understand exactly when the policy becomes active, how much the total term will cost, and what happens if a payment is late.

| Payment Structure | How It Usually Works | What to Check Before Buying |

|---|---|---|

| Monthly installments | The premium is split into monthly payments instead of being paid in full. | Ask about installment fees, due dates, late fees, payment method fees, and cancellation rules. |

| Low initial payment | The policy starts with a smaller first payment, followed by later payments. | Confirm the exact amount due today and whether later payments are higher than the first payment. |

| Premium financing | A finance company may pay the insurer, and the driver repays the finance company over time. | Review interest, finance charges, missed-payment rules, and whether the finance company can request cancellation for nonpayment. |

| Paid-in-full alternative | The driver pays the full policy term upfront. | Ask whether paying in full avoids installment fees or qualifies for a discount. |

Do not drive until the policy is bound, the required payment has been accepted, the start date is confirmed, and valid proof of insurance has been issued.

Payment Checklist Before You Buy

The safest way to compare BNPL-style car insurance is to treat the payment plan as one part of the policy, not the whole decision. A low first payment may help today, but the policy can become expensive or risky if the later payments, fees, or cancellation terms are unclear.

Confirm the exact payment required before the policy can start.

Compare the full six-month or annual cost, not only the first payment.

Ask about installment fees, late fees, service fees, and finance charges.

Confirm when proof is issued and when coverage actually starts.

Ask what happens if a payment fails or is paid late.

Review liability limits, deductibles, collision, comprehensive, and optional coverages.

What Coverage Should You Compare?

A flexible payment plan is only useful if the policy itself is strong enough. The Insurance Information Institute explains that auto insurance generally includes property coverage, liability coverage, and medical coverage. Property coverage can help with damage to or theft of the car, liability coverage can help with legal responsibility to others, and medical coverage can help with injury-related costs after an accident. [2]

| Coverage Type | What It Generally Does | Why It Matters With BNPL Payments |

|---|---|---|

| Liability coverage | Helps pay for injuries or property damage you cause to others, up to policy limits. | A low monthly payment may come with low limits, which can leave you exposed after a serious accident. |

| Collision coverage | Helps repair or replace your car after a covered collision, subject to the deductible. | Often required by lenders or leases and important if your car is expensive to repair or replace. |

| Comprehensive coverage | Helps with theft, vandalism, fire, hail, falling objects, and other non-collision losses. | Useful for newer, financed, leased, or higher-value vehicles. |

| Uninsured or underinsured motorist coverage | May help when another driver has no insurance or not enough insurance. | Can provide extra protection when another driver cannot fully pay for covered losses. |

| Medical payments or PIP | May help with accident-related medical costs, depending on state and policy terms. | Availability and requirements vary by state, so drivers should ask how it works locally. |

State minimum coverage may satisfy legal requirements, but it may not provide enough protection after a serious accident. The NAIC reminds consumers that auto policies are made up of different coverages and that there is no single policy officially called “full coverage.” [3]

How to Qualify for Flexible Payment Car Insurance

Eligibility varies by insurer, state, driver profile, vehicle, coverage level, payment method, and prior insurance history. Instead of assuming every driver qualifies for “pay later” terms, gather the right information and ask the insurer or agency what billing options are available.

Information usually needed for a quote

- Driver name, date of birth, license status, and driving history.

- Vehicle year, make, model, VIN, mileage, and ownership or lease status.

- Garaging ZIP code and how the vehicle is used.

- Current or prior insurance information, including any lapse history.

- Desired liability limits, deductibles, and optional coverages.

- Payment method and preferred billing schedule.

Benefits of BNPL-Style Car Insurance Payments

Flexible payments can help drivers who need coverage now but cannot comfortably pay the full premium upfront. This may be useful after buying a car, moving to a new state, replacing a canceled policy, or adding a driver to a household policy.

Potential advantages include:

- Starting required auto insurance without paying the full policy term upfront.

- Spreading premium costs across predictable monthly payments.

- Keeping cash available for registration, repairs, fuel, or emergency expenses.

- Making it easier to compare more than one policy option.

- Helping drivers avoid going uninsured when they need coverage quickly.

The benefit is strongest when the payment plan is affordable for the full term. A low first payment is not a good deal if the total cost is higher than expected or if the policy is likely to cancel after a missed installment.

Risks, Fees, and Cancellation Rules

Buy now pay later can make payments easier, but it can also create problems if the driver focuses only on the first payment. The CFPB says many BNPL loans do not charge interest, but most charge late fees if payments are not made on time. [4]

For car insurance, missed payments can be even more serious because a canceled policy can leave the driver without valid coverage. A lapse may lead to legal penalties, reinstatement fees, higher future rates, or denied claims if an accident happens after cancellation.

| Risk | Why It Matters | How to Reduce the Problem |

|---|---|---|

| Late fees | Missing a payment may add extra fees and make the policy harder to keep active. | Use reminders, autopay, or a due date that matches your pay schedule. |

| Coverage lapse | If the policy cancels, you may lose legal proof of insurance. | Ask how much notice is given before cancellation and how reinstatement works. |

| Higher total cost | Installment plans may include billing fees, service fees, interest, or finance charges. | Compare the full six-month or annual cost against paid-in-full pricing. |

| Weak coverage | A low payment may come from low liability limits or missing optional coverage. | Compare the coverage details, not just the monthly payment. |

| Confusing advertising | “Pay later” or “no deposit” may hide required first payments or fees. | Ask what amount is due before coverage starts and get confirmation in writing. |

How to Manage Payments and Avoid Late Fees

Managing payments is one of the most important parts of a BNPL-style auto policy. A flexible plan only helps if the driver can keep the policy active through the full term.

Payment management checklist

- Write down the due date for every installment.

- Ask whether autopay is required or optional.

- Confirm whether the payment date can match your paycheck schedule.

- Check whether debit card, credit card, bank transfer, or online payment options have fees.

- Review what happens if a payment fails.

- Keep proof of every payment and policy confirmation email.

Discounts That Can Lower the Total Cost

Discounts can sometimes lower the total premium more safely than cutting important coverage. The NAIC recommends comparing coverage carefully, reviewing optional coverages, and understanding what you are buying before choosing an auto insurance policy. [5]

| Discount or Strategy | How It May Help | What to Ask |

|---|---|---|

| Safe driver discount | May reduce premiums for drivers with clean records. | How many years of clean driving are required? |

| Good student discount | May help eligible students lower their premium. | What grades or documents are required? |

| Multi-policy discount | May lower cost when bundling auto with renters or homeowners insurance. | Is the bundled price actually cheaper than separate policies? |

| Telematics program | May reward safer driving or lower mileage. | Can my rate increase as well as decrease, and what data is collected? |

| Higher deductible | May lower collision or comprehensive premiums. | Could I afford the deductible after a claim? |

If you are also comparing broader auto coverage, review Young American auto insurance options to understand how coverage, discounts, and payment terms work together.

Telematics and Pay-As-You-Drive Options

Some drivers use telematics or usage-based insurance to try to lower premiums. The NAIC explains that usage-based insurance can track driving behavior through devices installed in a vehicle or through smartphones. These programs may measure miles driven, time of day, location, rapid acceleration, hard braking, hard cornering, cell phone usage, and other driving-related data. [6]

Telematics may help careful drivers, but it is not automatically the best option for everyone. Drivers should review privacy terms, whether rates can increase, how long monitoring lasts, and whether they can opt out later.

Before joining a telematics program, ask:

- What information is collected?

- Can the rate increase if my driving score is poor?

- Who can access the data?

- How long does monitoring last?

- Can I opt out later?

- Does the discount continue at renewal?

When BNPL Car Insurance May Make Sense

BNPL-style payment arrangements may make sense when a driver needs legal coverage quickly, has a realistic payment plan, understands the full cost, and can keep the policy active. It may not make sense if the driver is already struggling to cover monthly bills or if the quote only looks affordable because the coverage is too weak.

Simple decision rule

Choose flexible payments only if the policy meets legal requirements, includes the coverage you need, fits your monthly budget, and gives clear written terms for fees, due dates, cancellation, and proof of insurance.

Compare Flexible Car Insurance Payment Options

Flexible payments can help drivers start coverage, but the best policy is the one that balances affordability, active coverage, useful limits, and clear payment rules. Enter your ZIP code to begin comparing available options.

Frequently Asked Questions

Is buy now pay later car insurance real?

Yes, but it usually means a flexible payment structure rather than a special insurance product. Drivers may pay an initial amount and then make installments over time.

Is buy now pay later car insurance the same as no-deposit car insurance?

Not exactly. BNPL usually describes paying over time, while no-deposit advertising often describes a low upfront payment. In many cases, some payment is still required before coverage starts.

Can I get car insurance with no money down?

Some ads use “no money down” or “no deposit,” but many policies still require a first payment, fee, or approved billing arrangement before coverage starts. Always confirm what is due today.

Can missed BNPL payments cancel my insurance?

Yes. If you miss required insurance payments, the policy may cancel according to policy terms and state law. That can leave you without proof of insurance and may create legal or financial problems.

Does BNPL car insurance cost more?

It can. Installment plans may include billing fees, finance charges, late fees, or higher total costs than paying in full. Compare the full term cost before buying.

What should I compare before choosing BNPL car insurance?

Compare liability limits, deductibles, collision and comprehensive coverage, uninsured motorist options, payment fees, cancellation rules, discounts, and the exact date coverage starts.

This article is for general educational purposes and is not a personalized insurance recommendation. Auto insurance availability, payment options, required coverages, cancellation rules, and rates vary by state, insurer, driver profile, vehicle, and ZIP code. Always review the actual policy documents before buying coverage.

References

- [1] Consumer Financial Protection Bureau, “What is a Buy Now, Pay Later loan?” ConsumerFinance.gov ↩

- [2] Insurance Information Institute, “Auto insurance basics—understanding your coverage.” III.org ↩

- [3] National Association of Insurance Commissioners, “Consumer Shopping Tool for Auto Insurance.” NAIC.org ↩

- [4] Consumer Financial Protection Bureau, “Do Buy Now, Pay Later loans have fees?” ConsumerFinance.gov ↩

- [5] National Association of Insurance Commissioners, “A Shopping Tool for Auto Insurance.” NAIC.org ↩

- [6] National Association of Insurance Commissioners, “Want Your Auto Insurer to Track Your Driving? Understanding Usage-Based Insurance.” NAIC.org ↩