By Young Americans Insurance Editorial Team

Published on · Updated on

This Montana car insurance guide was reviewed for state minimum liability requirements, uninsured motorist information, quote-comparison usefulness, payment clarity, and consumer disclosure quality.

Editorial details

The Young Americans Insurance Editorial Team creates informational content about U.S. auto insurance requirements, coverage options, quote comparison, discounts, and payment considerations. This page is for general educational purposes only and does not replace advice from a licensed insurance professional.

Coverage availability, rates, discounts, deductibles, and payment terms vary by insurer, ZIP code, vehicle, driver profile, and selected coverage. Always review the actual policy documents before buying coverage.

Finding cheap car insurance in Montana starts with the state’s 25/50/20 liability requirement, but price should not be the only factor. A cheap policy can still be risky if it has weak liability limits, unclear payment terms, unaffordable deductibles, or missing protection for your own vehicle.

This guide explains Montana minimum requirements, uninsured motorist coverage, active insurance verification, local risk factors, discounts, city and driver-profile considerations, and smart ways to lower your premium without buying coverage that leaves you exposed.

Montana Car Insurance Requirements

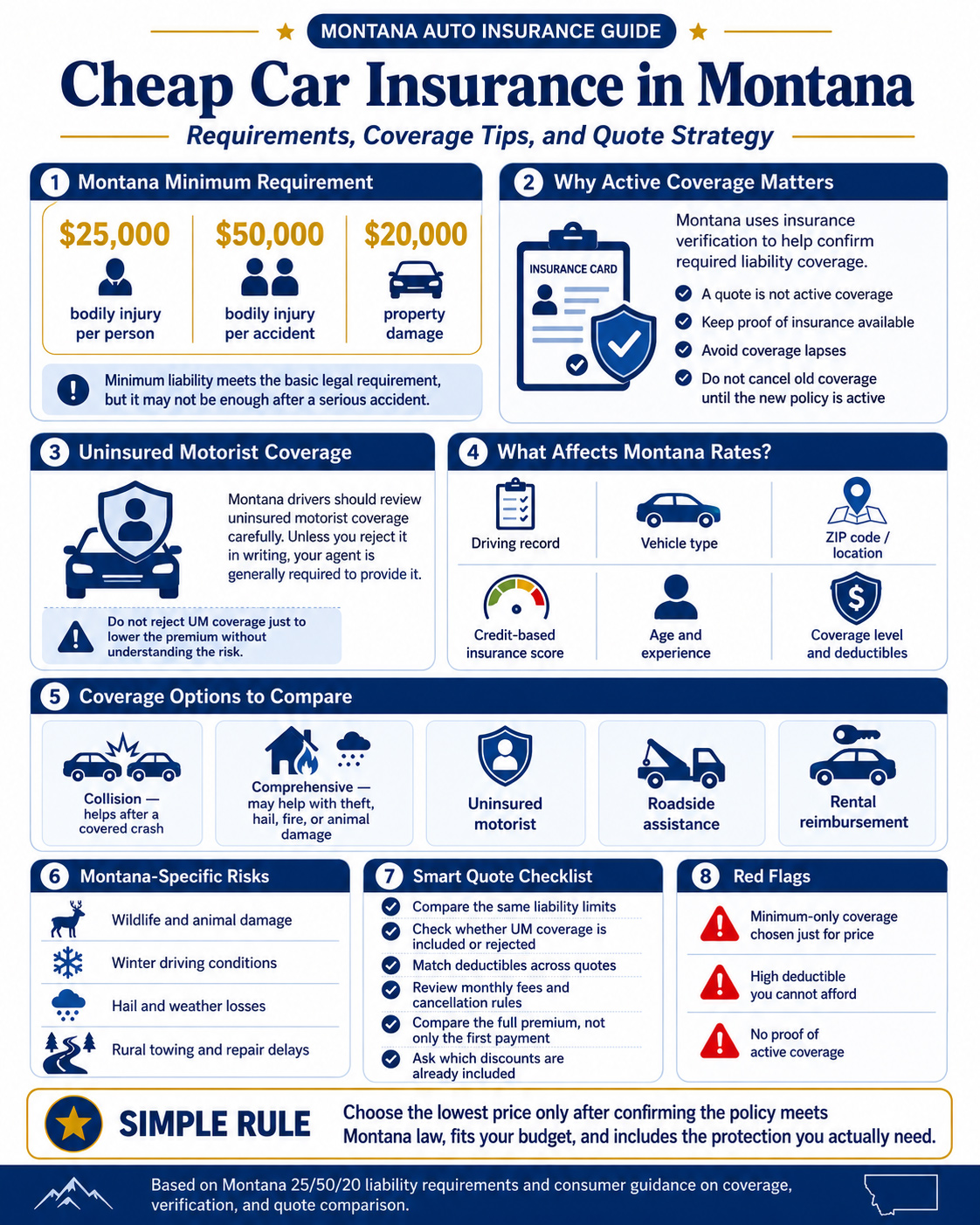

Montana drivers are required to carry liability insurance. Montana’s Motor Vehicle Division lists the minimum limits as $25,000 for bodily injury or death of one person, $50,000 for bodily injury or death of two or more people in one accident, and $20,000 for injury to or destruction of property of others.[1]

These limits are commonly written as 25/50/20. They can satisfy Montana’s basic legal requirement, but they may not fully protect a driver after a serious accident. Drivers with income, savings, assets, family drivers, newer vehicles, or long rural commutes should compare higher limits before choosing the cheapest quote.

25/50/20 minimum

Montana’s required liability limits are $25,000 per person, $50,000 per accident, and $20,000 property damage.

Minimum is not full protection

Liability helps others when you cause damage, but it does not automatically repair your own vehicle.

Active coverage matters

Montana uses insurance verification to help identify whether vehicles have required liability coverage.

Cheap Car Insurance in Montana: What “Cheap” Should Mean

The cheapest car insurance in Montana is not always the quote with the lowest first payment. A better goal is to find the lowest realistic price for coverage that keeps you legal, protects against the losses you cannot afford, and has payment terms you can maintain.

| Cheap Policy Feature | Why It Can Help | What to Watch |

|---|---|---|

| Minimum liability only | Usually lowers the premium because it includes less coverage. | Does not repair your car and may not be enough after a serious at-fault crash. |

| Higher deductible | Can lower collision or comprehensive premiums. | You must be able to pay the deductible after a claim. |

| Discount stacking | Good driver, multi-policy, multi-car, paperless, autopay, or good student discounts may reduce cost. | Some discounts require proof and may change at renewal. |

| Older paid-off vehicle | May allow liability-only coverage if you can afford to replace the car. | Dropping physical damage coverage shifts repair and replacement risk to you. |

| Monthly payment plan | Can make the policy easier to start. | Installment fees, late fees, and cancellation rules can raise the true cost. |

Compare the total six-month or annual premium, not just the first payment. Also compare the same limits, deductibles, drivers, vehicles, garaging ZIP code, and optional coverages on every quote.

Montana Minimum Liability Limits Explained

Liability coverage is the foundation of a Montana auto policy. It helps pay for injuries or property damage you cause to other people, up to your policy limits. It does not cover every possible loss, and it does not replace optional protection like collision, comprehensive, roadside assistance, or rental reimbursement.

| Montana Minimum Coverage | Required Limit | What It Generally Helps Cover |

|---|---|---|

| Bodily injury liability per person | $25,000 | Injury or death of one person when you are legally responsible for a covered accident. |

| Bodily injury liability per accident | $50,000 | Total injury or death claims for two or more people in one covered accident. |

| Property damage liability | $20,000 | Damage to another person’s vehicle, fence, building, or other property in a covered at-fault accident. |

If accident costs exceed your policy limits, you may be responsible for the remaining amount. Compare higher liability limits before choosing minimum-only coverage based only on price.

Montana Insurance Verification: Why Active Coverage Matters

Montana’s Motor Vehicle Division explains that the goal of its insurance verification system is to reduce the number of drivers who do not carry liability insurance as required by Montana law. The system supports real-time insurance verification and is designed to improve roadway safety.[2]

For drivers, the practical lesson is simple: a quote is not coverage, and a canceled policy can create problems. Keep proof of insurance available, make payments on time, and confirm that replacement coverage is active before canceling an existing policy.

Coverage continuity checklist

- Confirm the exact policy start date and time.

- Keep valid proof of insurance in the vehicle or accessible digitally where allowed.

- Do not cancel old coverage until the new policy is active.

- Update your insurer if your vehicle, drivers, address, or garaging location changes.

- Set reminders for monthly payments and renewal deadlines.

- Ask your insurer how quickly proof of coverage is available after binding.

Uninsured Motorist Coverage in Montana

Montana drivers should pay close attention to uninsured motorist coverage. Montana Code Annotated Section 33-23-201 addresses motor vehicle liability policies that include uninsured motorist coverage and the insured’s right to reject that coverage.[3]

The Montana Commissioner of Securities and Insurance explains that unless you sign a form stating you do not want uninsured motorist coverage, your agent is required by law to provide it to you.[4]

Ask what uninsured motorist coverage does, what limits are available, how much it costs, and what could happen if you are injured by a driver with no insurance. Do not reject it only to lower the premium without understanding the trade-off.

Minimum-Only vs. Better Protection

A minimum-only policy may be the cheapest way to satisfy Montana’s basic liability requirement, but it is not always the best financial choice. The right choice depends on your vehicle, savings, household drivers, commute, and risk tolerance.

| Policy Choice | What It Usually Includes | Risk to Consider |

|---|---|---|

| Minimum liability only | Montana’s 25/50/20 liability limits. | May not be enough after a serious crash and does not repair your own car. |

| Higher liability limits | More protection if you cause injuries or property damage to others. | Costs more than minimum coverage, but may better protect savings and income. |

| Liability plus UM coverage | Liability plus protection related to uninsured drivers, depending on policy terms. | Rejecting UM may lower price but can reduce protection after an accident with an uninsured driver. |

| Liability plus collision and comprehensive | Liability plus protection for your own vehicle after certain covered losses. | Costs more but can matter for newer, financed, leased, or hard-to-replace vehicles. |

What Montana Liability Insurance Does Not Cover

Liability insurance helps with damage or injuries you cause to others. It generally does not pay for damage to your own car, your own repairs after an at-fault crash, non-collision losses, or rental car costs after a claim unless you bought additional coverage.

| Loss or Situation | Does Minimum Liability Usually Help? | Coverage to Compare |

|---|---|---|

| Your own car is damaged in an at-fault crash | No. | Collision coverage. |

| Your vehicle is stolen, vandalized, damaged by hail, or hit by a falling object | No. | Comprehensive coverage. |

| You hit wildlife or an animal damages your vehicle | No. | Comprehensive coverage, depending on policy terms. |

| Your car is in the shop after a covered claim and you need temporary transportation | No. | Rental reimbursement coverage. |

| Your vehicle breaks down far from home | No. | Roadside assistance or towing coverage. |

Optional Coverage Montana Drivers Should Compare

The cheapest Montana policy may be liability-only, but that does not mean it is the best fit. Montana drivers should review vehicle value, savings, commute distance, household drivers, weather exposure, wildlife risk, and any lender or lease requirements before removing optional coverage.

| Coverage Option | What It Generally Does | Why It May Matter in Montana |

|---|---|---|

| Collision coverage | Helps repair or replace your own vehicle after a covered collision, subject to the deductible. | Useful for financed, leased, newer, or higher-value vehicles. |

| Comprehensive coverage | Helps with non-collision losses such as theft, vandalism, fire, hail, falling objects, and animal damage. | Can matter because weather, wildlife, and rural conditions can make non-collision losses expensive. |

| Uninsured motorist coverage | May help when another driver has no insurance. | Understand Montana’s offer/rejection rules before signing a rejection. |

| Medical payments coverage | May help with accident-related medical expenses, depending on policy terms. | Can provide extra support regardless of who caused the crash, subject to limits. |

| Roadside assistance | May help with towing, lockouts, dead batteries, or flat tires. | Useful for rural driving, long distances, winter conditions, or older vehicles. |

| Rental reimbursement | May help pay for a rental car while your vehicle is repaired after a covered claim. | Helpful if you rely on your vehicle for work, school, or family transportation. |

Montana-Specific Risks to Consider

Montana has rural highways, winter driving conditions, long distances, wildlife exposure, hail risk, and areas where repair or towing may take longer than in dense urban markets. These local factors can make optional coverages more valuable for some drivers.

Ask whether comprehensive coverage applies to animal-related damage and how the deductible works.

Roadside assistance and towing coverage can matter if you regularly drive long distances or rural routes.

Comprehensive coverage may help with covered weather-related vehicle damage, subject to policy terms.

Rental reimbursement can help if your car is repaired after a covered claim and you need transportation.

Factors Affecting Car Insurance Rates in Montana

Auto insurance rates are personalized. The Insurance Information Institute explains that factors such as driving record, vehicle use, location, age, gender, vehicle type, credit, and coverage choices can affect auto insurance pricing.[5]

| Rate Factor | Why It Matters in Montana | What Drivers Can Do |

|---|---|---|

| Where you live | Traffic, theft risk, claim frequency, weather, repair costs, and local road conditions can affect premiums. | Use the correct garaging address and compare quotes after moving. |

| Driving record | Tickets, at-fault accidents, DUI history, and claims can increase rates. | Maintain a clean record and ask when past incidents may stop affecting pricing. |

| Vehicle type | Repair cost, value, safety features, theft risk, and vehicle use influence premiums. | Compare insurance quotes before buying a car, truck, or SUV. |

| Credit-based insurance score | Montana’s insurance department says insurers may use aspects of credit to create an insurance credit score. | Ask whether credit affected your rate and compare again if your credit improves.[6] |

| Age and driving experience | Younger or newer drivers often pay more because they have less driving history. | Ask about good student, driver training, safe driver, or family-policy discounts. |

| Coverage level | Higher limits and optional coverage cost more but can reduce financial risk after a loss. | Compare the same limits and deductibles across every quote. |

Cheap Montana Car Insurance by Driver Situation

Different Montana drivers should compare coverage differently. A student in Missoula, a family in Billings, a commuter near Bozeman, and a rural driver outside Great Falls may not need the same limits, deductibles, or optional coverages.

| Driver Situation | Smart Savings Focus | Coverage Warning |

|---|---|---|

| Young driver or student | Ask about good student, driver education, family policy, telematics, and safe-vehicle discounts. | Do not reduce liability too far just to lower the monthly payment. |

| Driver with an older paid-off car | Compare liability-only against liability plus comprehensive if wildlife, hail, or theft risk matters. | Dropping collision means you pay for your own at-fault crash repairs. |

| Rural or long-distance driver | Compare roadside assistance, towing, comprehensive, and rental reimbursement. | A cheaper policy may be less useful if a claim leaves you without transportation. |

| Homeowner or renter | Ask about bundling auto with home, condo, or renters insurance. | Bundling is not always cheaper than separate policies, so compare both. |

| Driver with tickets or prior claims | Compare multiple insurers, keep coverage active, and ask when violations stop affecting your rate. | A lapse can make future coverage harder or more expensive. |

How to Find Cheap Car Insurance in Montana

The best way to find cheaper Montana car insurance is to compare multiple quotes using the same coverage details. The National Association of Insurance Commissioners recommends comparison shopping, reviewing coverage, checking deductibles, and asking about discounts when shopping for auto insurance.[7]

Quote comparison checklist

- Use the same drivers, vehicles, garaging address, and mileage estimate.

- Compare the same liability limits on every quote.

- Confirm whether uninsured motorist coverage is included or rejected.

- Check whether collision and comprehensive are included.

- Use the same deductibles across quotes.

- Review monthly fees, late fees, and cancellation rules.

- Compare the full six-month or annual premium, not only the first payment.

- Ask which discounts are included and which still require proof.

Young drivers can also review cheap car insurance for young drivers for more savings strategies related to good student discounts, safe vehicles, family policies, and telematics.

Discounts Montana Drivers Should Ask About

Discounts can make a major difference, especially when several apply at the same time. Availability varies by insurer, so ask for a full discount review before lowering coverage.

Common discounts to ask about

- Multi-policy discount for bundling auto with renters, condo, or homeowners insurance.

- Multi-vehicle discount for insuring more than one vehicle on the same policy.

- Good driver or accident-free discount for a clean record.

- Good student discount for eligible young drivers.

- Defensive driving or driver education discount where available.

- Safety feature or anti-theft discount for qualifying vehicles.

- Paid-in-full, paperless, autopay, or electronic document discount.

- Usage-based or telematics discount for drivers who qualify.

Cheap Montana Car Insurance Red Flags

A cheap quote can be useful, but it can also hide weak coverage or risky payment terms. Before choosing the lowest price, make sure the quote actually fits your situation.

25/50/20 may satisfy Montana law, but it may not be enough after a serious accident.

Do not sign a UM rejection only to lower the premium without understanding the risk.

A higher deductible can lower premium but create a financial problem after a claim.

A quote is not enough. Confirm the policy is active and proof of insurance is available.

Should You Choose a National or Regional Insurer?

Montana drivers may compare national insurers, regional carriers, mutual companies, and local agencies. The cheapest company can change depending on the driver, vehicle, coverage level, location, credit-based insurance score, and discount eligibility.

| Option | Potential Advantage | What to Check |

|---|---|---|

| National insurer | May offer strong digital tools, broad availability, and multiple discounts. | Claims support, rate competitiveness, and local repair network. |

| Regional insurer | May understand Montana roads, rural driving, weather, and local service needs. | Financial strength, complaint history, and coverage options. |

| Local agent | Can help explain policy terms and compare multiple companies. | Whether the agent represents one insurer or multiple insurers. |

| Direct online quote | Can be fast and convenient for price comparison. | Whether the quote is final, complete, and based on accurate information. |

Drivers with flexible payment needs can also compare low down payment car insurance options and ask whether monthly payments, paid-in-full discounts, or installment fees change the total cost.

Before You Buy: Montana Car Insurance Checklist

Before buying a policy, confirm that the quote is not only cheap but also valid, complete, and realistic for your driving needs.

Before paying, confirm:

- The policy meets Montana’s 25/50/20 minimum liability requirement.

- The policy start date and proof of insurance timing are clear.

- Uninsured motorist coverage is included or you understand the rejection form.

- All household drivers and vehicles are listed correctly.

- Collision and comprehensive are included if required by a lender or lease.

- The deductible is an amount you can afford after a claim.

- Monthly payments, installment fees, late fees, and cancellation terms are clear.

- The total six-month or annual premium is compared, not only the first payment.

Compare Montana Car Insurance Before You Buy

The cheapest Montana policy should still meet legal requirements, include practical protection, and fit your monthly budget. Enter your ZIP code to begin comparing available auto insurance options.

Frequently Asked Questions

What is the minimum car insurance required in Montana?

Montana requires minimum liability limits of 25/50/20: $25,000 bodily injury or death per person, $50,000 bodily injury or death per accident, and $20,000 property damage per accident.

Is minimum liability enough in Montana?

Minimum liability can satisfy the basic legal requirement, but it may not be enough after a serious accident. Higher limits may be worth comparing if you have income, savings, assets, family drivers, or long commutes.

Does Montana require uninsured motorist coverage?

Montana law addresses uninsured motorist coverage and the insured’s right to reject it. Montana CSI explains that unless you sign a form stating you do not want uninsured motorist coverage, your agent is required by law to provide it to you.

How can Montana drivers lower car insurance costs?

Compare quotes, keep a clean driving record, ask about discounts, review deductibles, choose a practical vehicle, avoid lapses, and compare the full policy cost instead of only the monthly payment.

Should I drop collision and comprehensive on an older car?

It may make sense if the car has low value and is paid off, but consider whether you could afford repairs or replacement after an at-fault crash, theft, hail, vandalism, fire, or animal damage.

Why does Montana insurance verification matter?

Montana’s insurance verification system helps confirm whether vehicles have required liability coverage. Drivers should keep coverage active and avoid relying on a quote before the policy is bound.

Final Thoughts on Cheap Car Insurance in Montana

To find cheap car insurance in Montana, start with the 25/50/20 legal requirement, then compare whether higher liability limits, uninsured motorist coverage, collision, comprehensive, roadside assistance, or rental reimbursement are worth the additional cost.

The cheapest policy is only a good deal if it keeps you legal, fits your deductible budget, has clear payment terms, and protects you from the losses you cannot afford yourself.

References

- Montana Motor Vehicle Division, Vehicle Insurance and Verification. Source ↩

- Montana Motor Vehicle Division, Vehicle Insurance and Verification. Source ↩

- Montana Code Annotated, Section 33-23-201, Motor Vehicle Liability Policies to Include Uninsured Motorist Coverage — Rejection by Insured. Source ↩

- Montana Commissioner of Securities and Insurance, Auto Insurance. Source ↩

- Insurance Information Institute, What Determines the Price of My Auto Insurance Policy? Source ↩

- Montana Commissioner of Securities and Insurance, Auto Insurance. Source ↩

- National Association of Insurance Commissioners, Tips for Saving on Your Auto Insurance. Source ↩