By Young Americans Insurance Editorial Team

Published on · Updated on

Car insurance in Alabama starts with one basic rule: drivers need valid liability coverage or another approved form of financial responsibility before operating a vehicle. But buying only the state minimum is not always the smartest financial choice.

This guide explains Alabama’s minimum liability requirements, what those limits do and do not cover, how registration suspension can happen, and what Alabama drivers should compare before choosing a policy.

Alabama Car Insurance Requirements

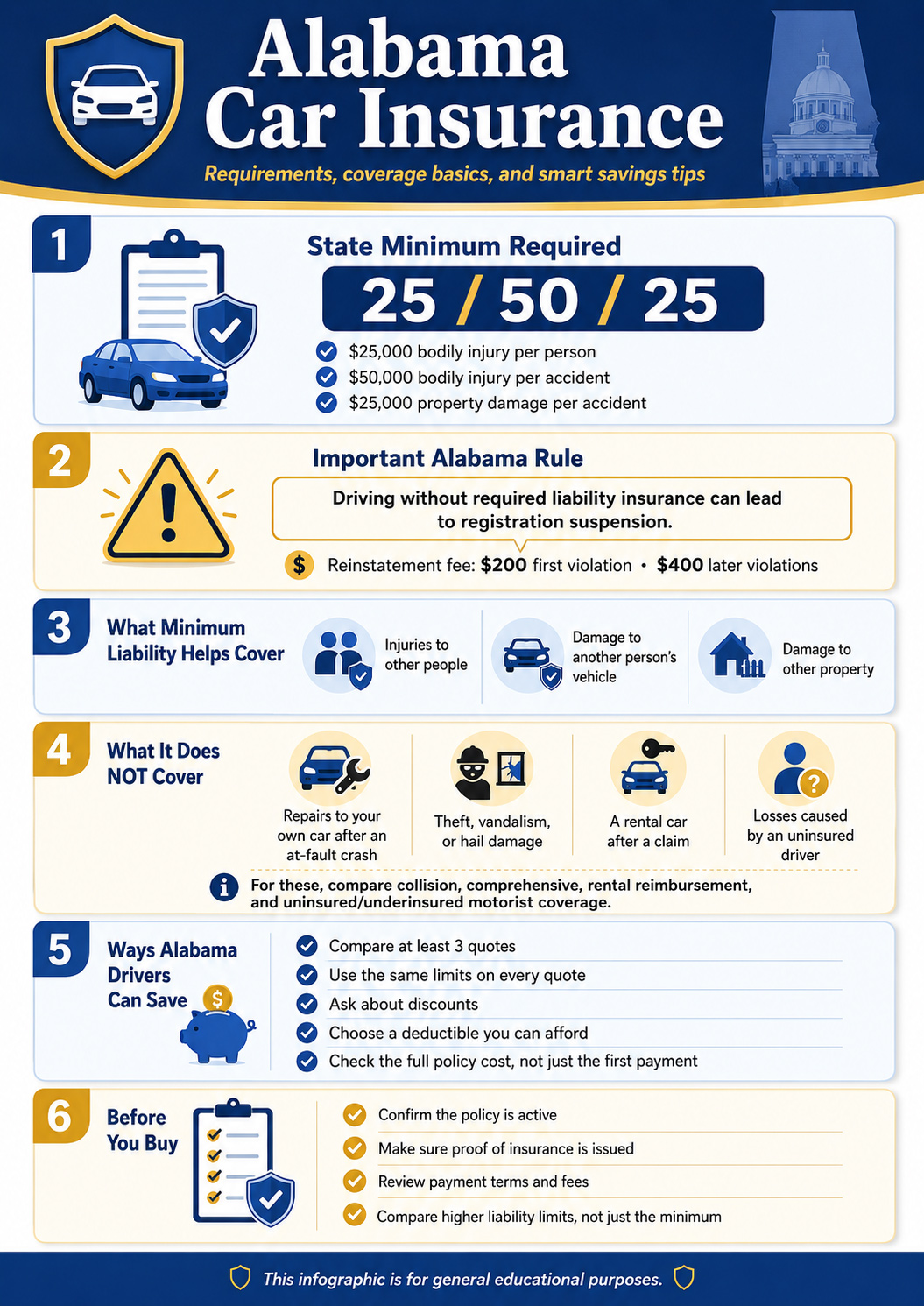

Alabama drivers are required to maintain mandatory liability insurance or another accepted form of financial responsibility. The Alabama Department of Insurance describes the state minimum auto liability limits as 25/50/25: $25,000 for bodily injury liability per person, $50,000 maximum for bodily injuries in one accident, and $25,000 for property damage per accident.[1]

Alabama’s Mandatory Liability Insurance system is also tied to vehicle registration. The Alabama Department of Revenue states that if a vehicle is determined not to be insured according to the MLI law, the department will suspend the motor vehicle registration. The reinstatement fee is listed as $200 for a first violation and $400 for subsequent violations, with proof of current liability insurance required.[2]

Legal minimum

Alabama’s minimum liability requirement is commonly written as 25/50/25.

Proof matters

A quote is not active coverage. Drivers should wait until the policy is bound and proof of insurance is issued.

Minimum is not full protection

Minimum liability may satisfy the law, but it may not fully protect your finances after a serious crash.

Minimum Liability Coverage in Alabama

Liability coverage helps pay for injuries or property damage you cause to other people, up to your policy limits. It does not automatically repair your own car after an at-fault crash, theft, hail, flood, vandalism, falling objects, or other physical damage loss.

| Alabama Minimum Coverage | Required Limit | What It Generally Helps Cover |

|---|---|---|

| Bodily injury liability per person | $25,000 | Injury or death of one person when you are legally responsible for a covered accident. |

| Bodily injury liability per accident | $50,000 | Total injury or death claims for two or more people in one covered accident. |

| Property damage liability | $25,000 | Damage to another person’s vehicle, fence, building, or other property in a covered accident. |

Alabama’s minimum liability limits can keep a driver compliant with the basic state requirement, but higher limits may be worth comparing if you have income, savings, a long commute, a financed vehicle, or household drivers to protect.

What Alabama Minimum Liability Does Not Cover

The biggest mistake many drivers make is assuming that “full legal coverage” means the same thing as “full financial protection.” Alabama’s minimum liability coverage is mainly designed to protect other people when you cause a covered accident. It is not designed to cover every cost you may face after a crash.

| Situation | Does Minimum Liability Usually Help? | Coverage to Compare |

|---|---|---|

| You damage another driver’s car | Yes, up to the property damage liability limit. | Higher property damage liability limits. |

| Your own car is damaged in an at-fault accident | No, not under liability-only coverage. | Collision coverage. |

| Your car is stolen, vandalized, or damaged by hail | No, not under liability-only coverage. | Comprehensive coverage. |

| You are hit by a driver with no insurance or too little insurance | Not through your own liability coverage. | Uninsured or underinsured motorist coverage. |

| You need a rental car after a covered claim | No, unless you bought rental reimbursement. | Rental reimbursement coverage. |

How to Find Affordable Car Insurance in Alabama

Affordable car insurance is not only the lowest monthly payment. A policy can look cheap because it has low liability limits, high deductibles, limited optional coverage, installment fees, or missing household drivers. When comparing cheap car insurance options with flexible payments, use the same coverage limits and deductibles on each quote so the comparison is fair.

Smart quote comparison checklist

- Compare at least three quotes using the same liability limits.

- Check whether collision and comprehensive coverage are included or excluded.

- Review deductibles and make sure you could afford them after a claim.

- Ask about monthly installment fees, late fees, cancellation rules, and down payment requirements.

- Confirm whether the quote includes all household drivers who should be listed.

- Ask which discounts are included and which discounts require proof.

- Compare the full six-month or annual cost, not only the first payment.

Alabama Driver Scenarios: What to Compare

Different Alabama drivers need different quote comparisons. A minimum-only policy may be enough for one driver, while another driver may need higher limits, physical damage coverage, or flexible payment options.

Compare liability-only quotes, but also price higher limits. Sometimes moving above the state minimum costs less than expected.

Your lender may require collision and comprehensive coverage. Do not buy liability-only coverage if your loan or lease requires physical damage protection.

Compare vehicle choice, good student discounts, driver training discounts, and household policy options. Vehicle repair cost can strongly affect premiums.

A lapse can make quotes more expensive. Focus on getting active coverage, keeping payments current, and comparing again after maintaining continuous insurance.

Coverage Options Alabama Drivers Should Understand

State minimum liability coverage is only one part of an auto policy. Drivers who want stronger protection should compare optional coverages based on vehicle value, financing status, savings, commute, and risk tolerance.

| Coverage Option | What It Generally Does | Why Alabama Drivers Compare It |

|---|---|---|

| Collision coverage | Helps repair or replace your car after a covered collision, subject to the deductible. | May be required if the vehicle is financed or leased. |

| Comprehensive coverage | Helps with non-collision losses such as theft, vandalism, fire, hail, falling objects, or certain weather events. | Useful if you cannot afford to replace the car after a non-crash loss. |

| Uninsured or underinsured motorist coverage | May help when another driver has no insurance or not enough insurance. | Can add protection when another driver cannot fully pay for your losses. |

| Medical payments coverage | May help with medical expenses after a covered accident, depending on policy terms. | Can provide extra support regardless of who caused the crash, subject to limits. |

| Rental reimbursement | May help pay for a rental car while your covered vehicle is repaired after a covered claim. | Helpful if you rely on your car for work, school, or family needs. |

| Roadside assistance | May help with towing, jump starts, lockouts, or flat tires, depending on the plan. | Useful for long commutes, older vehicles, or rural driving. |

Practical Ways to Save on Alabama Car Insurance

Saving money starts with comparison shopping, but the policy still has to protect you. The National Association of Insurance Commissioners recommends reviewing coverage, deductibles, discounts, and total premium when shopping for auto insurance.[3]

Ways to lower the total cost

- Maintain a clean driving record by avoiding tickets, at-fault accidents, and coverage lapses.

- Ask about safe driver, good student, driver training, paperless billing, automatic payment, and multi-policy discounts.

- Choose a safe, practical vehicle that is not unusually expensive to repair or insure.

- Raise deductibles only if you have enough savings to pay them after a claim.

- Bundle auto and home or renters insurance only when the combined cost is actually lower.

- Review coverage after moving, buying a car, paying off a loan, or adding a driver.

- Compare the same policy structure across companies instead of comparing a bare-minimum quote to a fuller policy.

Deductibles, Credit, and Vehicle Choice

Several factors can affect what Alabama drivers pay. Insurers may consider driving record, vehicle type, location, mileage, coverage choices, deductible levels, prior coverage, and credit-based insurance scores where allowed by state law. The NAIC explains that many auto and homeowners insurers use credit-based insurance scores in underwriting and rating, although the way these tools are regulated can vary by state.[4]

| Factor | How It Can Affect Price | What You Can Do |

|---|---|---|

| Deductible | A higher deductible may reduce premium for collision or comprehensive coverage. | Choose a deductible you can realistically pay after a claim. |

| Driving record | Tickets, at-fault accidents, and claims can increase rates. | Drive safely and ask when violations may stop affecting your quote. |

| Vehicle type | Repair cost, safety features, theft risk, and vehicle value can affect pricing. | Compare insurance costs before buying a vehicle. |

| Credit-based insurance score | Some insurers may use it as one rating factor where permitted. | Pay bills on time, check reports for errors, and compare multiple companies. |

| Location | ZIP code, traffic, theft, weather, and claim frequency can influence rates. | Update your address accurately and compare quotes after moving. |

If you are shopping for a teen or new driver, choosing one of the cheapest cars to insure for teens can make a meaningful difference because vehicle value, safety, and repair costs can affect premiums.

Flexible Payments and BNPL-Style Options

Some drivers want a policy with a manageable first payment instead of paying the full premium upfront. That can help with budgeting, but Alabama drivers should still compare the full policy cost, installment fees, and cancellation rules. A low first payment is not useful if the policy cancels quickly after a missed installment.

Drivers comparing BNPL-style car insurance payment options should ask when coverage starts, what amount is due today, what each monthly payment will be, and whether proof of insurance is issued immediately after binding.

Payment rule to remember

Never assume a quote equals active coverage. Wait until the policy is bound and you have valid proof of insurance before driving.

When Alabama Drivers Should Review Their Policy

A policy that fit last year may not fit today. Review your car insurance after moving, buying or selling a vehicle, changing jobs, adding a driver, paying off a loan, getting married, or improving your driving record. Coverage reviews can reveal discounts, errors, unnecessary extras, or gaps that were easy to miss when the policy was first purchased.

Review your policy when:

- You move to a new ZIP code or county.

- You add or remove a household driver.

- You buy, sell, finance, or pay off a vehicle.

- Your commute or annual mileage changes.

- You complete a driver safety course.

- Your credit or driving record improves.

- Your vehicle is older and collision or comprehensive coverage may need review.

Alabama Car Insurance Buying Checklist

Before you buy a policy, make sure the quote matches what you actually need. The cheapest option may work for some drivers, but it should not hide missing coverage, unrealistic deductibles, or payment terms that make cancellation more likely.

| Question to Ask | Why It Matters |

|---|---|

| Does this quote meet Alabama’s minimum liability requirement? | You need at least the required liability coverage or another approved form of financial responsibility. |

| Are the liability limits higher than the state minimum? | Higher limits may provide better financial protection after a serious accident. |

| Does the policy include collision and comprehensive? | These coverages are important if you want protection for damage to your own vehicle. |

| What is due today, and what are the future payments? | A low first payment can still lead to a high total cost if fees or installments are expensive. |

| When does coverage start? | You should not drive until the policy is active and proof of insurance is available. |

Compare Alabama Car Insurance Before You Buy

The cheapest Alabama policy is not always the best. Compare liability limits, deductibles, optional coverages, payment terms, discounts, and claims support before making a decision.

Compare Affordable Car Insurance OptionsFrequently Asked Questions About Alabama Car Insurance

What is the minimum car insurance required in Alabama?

Alabama’s minimum liability limits are commonly described as 25/50/25: $25,000 bodily injury per person, $50,000 for all bodily injuries in one accident, and $25,000 property damage per accident.

Can Alabama suspend my registration for no insurance?

Yes. Alabama Revenue states that if a vehicle is determined not to be insured according to the Mandatory Liability Insurance law, the department will suspend the motor vehicle registration.

Is minimum liability enough in Alabama?

Minimum liability can satisfy the legal requirement, but it may not be enough after a serious accident. Compare higher limits if you have income, savings, assets, a long commute, or household drivers to protect.

How can Alabama drivers lower car insurance costs?

Compare quotes, keep a clean record, ask about discounts, choose a practical vehicle, avoid coverage lapses, review deductibles, and compare the full policy cost instead of only the monthly payment.

Should I buy liability-only car insurance in Alabama?

Liability-only coverage may be enough for some older vehicles, but it does not repair your own car after an at-fault crash or many non-collision losses. If your vehicle is financed, leased, or difficult to replace, compare collision and comprehensive coverage too.

Do Alabama drivers need proof of insurance?

Yes. Drivers should keep valid proof of insurance after the policy is active. A quote or application is not the same as active coverage.

References

- Alabama Department of Insurance, Automobile Insurance FAQs. Source ↩

- Alabama Department of Revenue, Mandatory Liability Insurance. Source ↩

- National Association of Insurance Commissioners, Tips for Saving on Your Auto Insurance. Source ↩

- National Association of Insurance Commissioners, Credit-Based Insurance Scores. Source ↩